The Innovation - Inflation Race

The Innovation - Inflation Race

Innovation has started to re-ignite productivity and prosperity; but out-of-control fiscal policy gives inflation an extra boost.

In my previous blog on GE’s heartbreaking breakup I discussed GE’s innovation strategy, centered on diversification and internal synergies, and compared it to an approach based on external ecosystem synergies. For a company, innovation can be crucial to business success; for a country, it plays a key role in shaping the macroeconomic environment.

Innovation—to come to another burning issue—could also be the silver bullet against the inflation vampire. By boosting productivity, innovation can help offset pressure from rising wages and other input costs. If workers are more productive, employers can grant higher compensation without having to raise product prices by a commensurate amount. If innovation helps simplify the production process, limit waste, reduce the use of materials or switch to cheaper ones, firms can absorb a rise in input costs without a proportionate increase in prices.

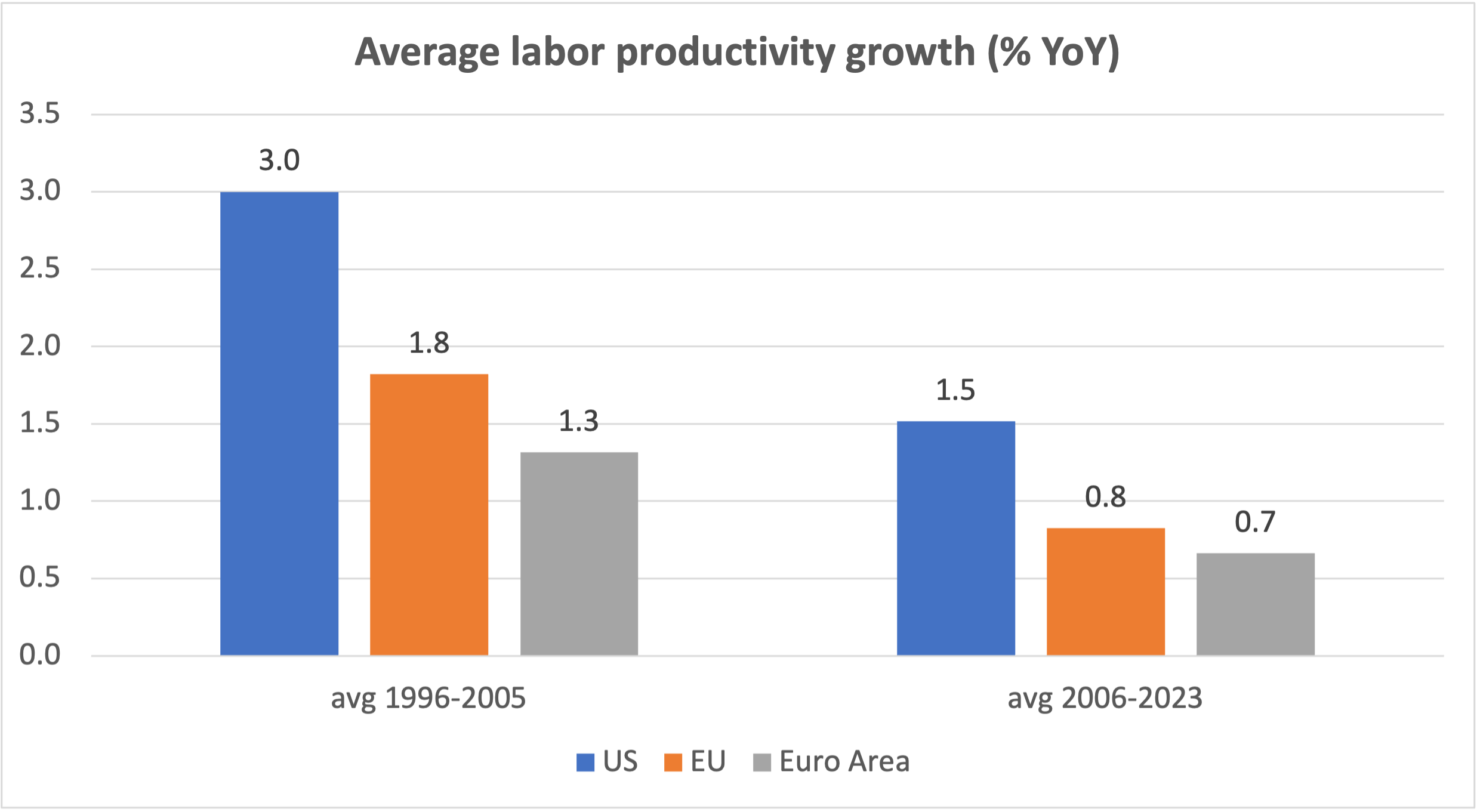

Stagnation

For the past twenty years, productivity growth across advanced economies had settled at a depressingly weak pace, as I have shown in a previous blog. Engineers and scientists kept beavering away, thought leaders and talking heads kept hyping the wonders of digital innovation, but productivity languished. This fed the ‘secular stagnation’ narrative, a dispiriting tale depicting an endless future of crawling living standards.

Source: OECD

The apparent ineffectiveness of private sector-led innovation shifted the focus towards government intervention. Economic stagnation implies fewer opportunities for people to move up the income ladder, and provides greater justification for income redistribution policies. The secular stagnation hypothesis itself argued that only government could reboot economic growth through a burst of public spending, preferably concentrated on public investment. Governments were all too happy to go along, spending lavishly and boosting public debt stocks to record levels. Inflation seemed to be forgotten, a ghost of the past—until it came back with a vengeance.

Acceleration

Then, over the latter part of 2023, US productivity enjoyed a marked acceleration. Not quite back to the sparkling 3% annual average of the 1996-2005 ‘golden age’, but still the pace stepped up from 1.2% in the second quarter to 2.6% in the last quarter of the year.

Source: OECD

Productivity statistics can be very volatile, so it’s too early to say if we have reached a stronger growth plateau; but three consecutive quarters of acceleration are encouraging. Moreover, as I noted,

over the past decade, companies have been carrying out a massive effort in adopting new digital technologies. And while there has been plenty of hype, a lot of important innovation has taken place, and it would be surprising if none of it ever resulted in some boost to productivity.

So let’s be optimistic and assume that productivity growth is stepping onto a higher plateau. Maybe something in the 2-2.5% range, which would still be a great improvement over the lackluster 1.5% of the past 18 years.

The good news is that faster productivity growth, compounded over time, makes a big difference to living standards. If advanced economies had managed to maintain the quicker productivity growth pace even after 2006, their economies would now be almost one-third larger, and living standards correspondingly higher.

Inflation

The bad news is that faster productivity growth by itself is unlikely to bring inflation back to the 2% target. The reason ties back to the debate on whether inflation has been mostly a supply or a demand problem—and to its sectoral distribution.

The initial surge in prices, with inflation rates close to 10%, reflected supply and demand both moving away from each other. Supply was strangled by supply chain disruptions and an energy shock (Russia’s invasion of Ukraine), while demand was boosted by a flamboyant fiscal stimulus. Supply shocks have since abated, and the acceleration in productivity growth has helped ease production constraints—much like the increase in the labor force, helped by immigration.

Demand, however, has continued to power ahead, in part thanks to accumulated household savings, but largely because fiscal policy remains recklessly expansionary for an economy already at full employment. The Congressional Budget Office projects a fiscal deficit of 5 1/2 % of GDP this year, rising back to over 6% in 2025 and remaining in a 5-6% of GDP range for the next ten years. Supply has hurried back towards demand, but demand keeps running away.

Source: Congressional Budget Office

Fiscal policy contributes to higher inflation in two ways. First, by boosting current demand for goods and services. Second, by increasing the risk that monetary policy will eventually need to monetize the government’s financing needs. This is not an academic concern: we have already witnessed this phenomenon at scale, with massive and protracted Quantitative Easing. Unless and until fiscal policy comes back to earth, it will be hard to bring inflation pressures fully and durably under control.

Supply has hurried back towards demand, but demand keeps running away.

At your service

The other issue has to do with sector differences. Services tend to have lower productivity levels and growth rates than manufacturing (see for example this OECD study); and many of the most promising digital-industrial innovations are…well…in industry, helping produce goods more efficiently. Inflation pressures now are instead concentrated in services. We do not have timely quarterly data on sector-level productivity to settle the question, but the evidence indicates that innovation is not boosting services supply enough to keep up with demand. Maybe Artificial Intelligence one day will bring the productivity growth potential of services on a par with goods; but we’re not there yet.

It’s time for policymakers to show more faith in innovation and give up on unsustainable fiscal stimulus.