Rising Yields And Sinking Theories

A reality check after the Secular Stagnation delusion

The recent synchronized rise in government bond yields across advanced economies has raised concern. Some fear it could sabotage growth; others that it might be a harbinger of financial instability. Many characterize it as unexpected, remarkable, and somewhat alarming.

What is remarkable is that it came as a surprise. US real GDP growth is running at around 2.5%, and headline inflation averaged close to 3% for over two years even before the current energy shock…what would you expect bond yields to do?

Secular delusion

The reason it did come as a surprise, I think, is that during much of the past two decades we seem to have lost perspective, lost our grip on reality. The Secular Stagnation delusion is perhaps the best example.

In 2013, Harvard’s Larry Summers dusted off Secular Stagnation to argue that we were destined to live with weak growth, low inflation, and extremely low interest rates for the foreseeable future. In 2023, as interest rates rose on the back of the inflation surge, MIT’s Olivier Blanchard invoked Secular Stagnation to predict they would soon fall again, because three structural drivers would continue to cause weak growth and excess savings for the foreseeable future:

Aging populations saving more for a longer retirement;

Higher global uncertainty fueling demand for safe assets;

Depressed real investment.

I pushed back against Summers and Blanchard at the time, and the current rise in yields gives a good opportunity to revisit and update the arguments.

The starting observation which triggered the search for secular forces was the long-term decline in interest rates. The chart below shows the 10-year UST yield on a downward trend beginning in the 1980s through the Covid pandemic.

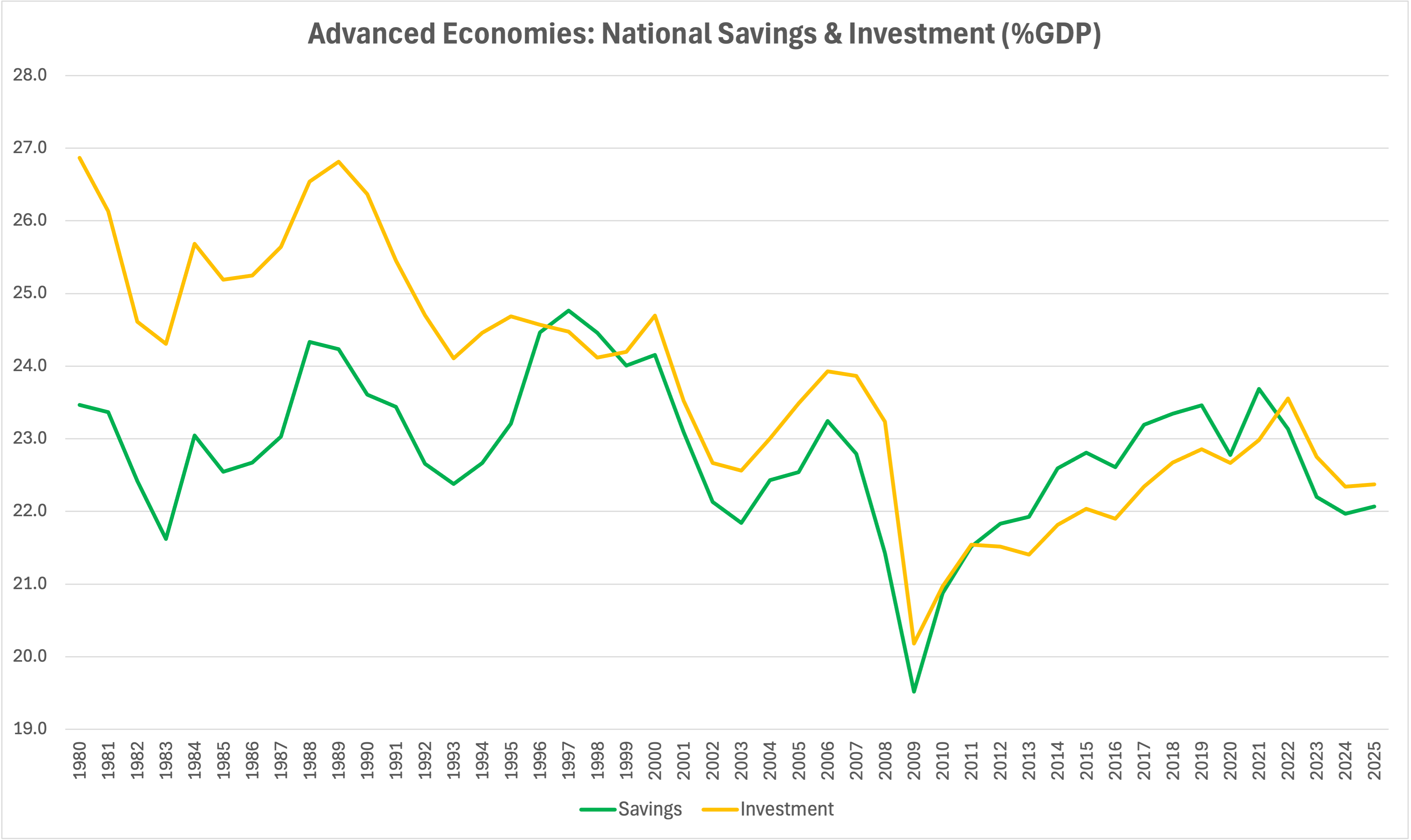

Savings glut

Was it driven by a savings glut? Looking at the numbers, I’d say it’s doubtful. In advanced economies, between 1980 and 2011 real investment exceeded savings. There were some excess savings between 2012 and 2021, but they’ve disappeared already.

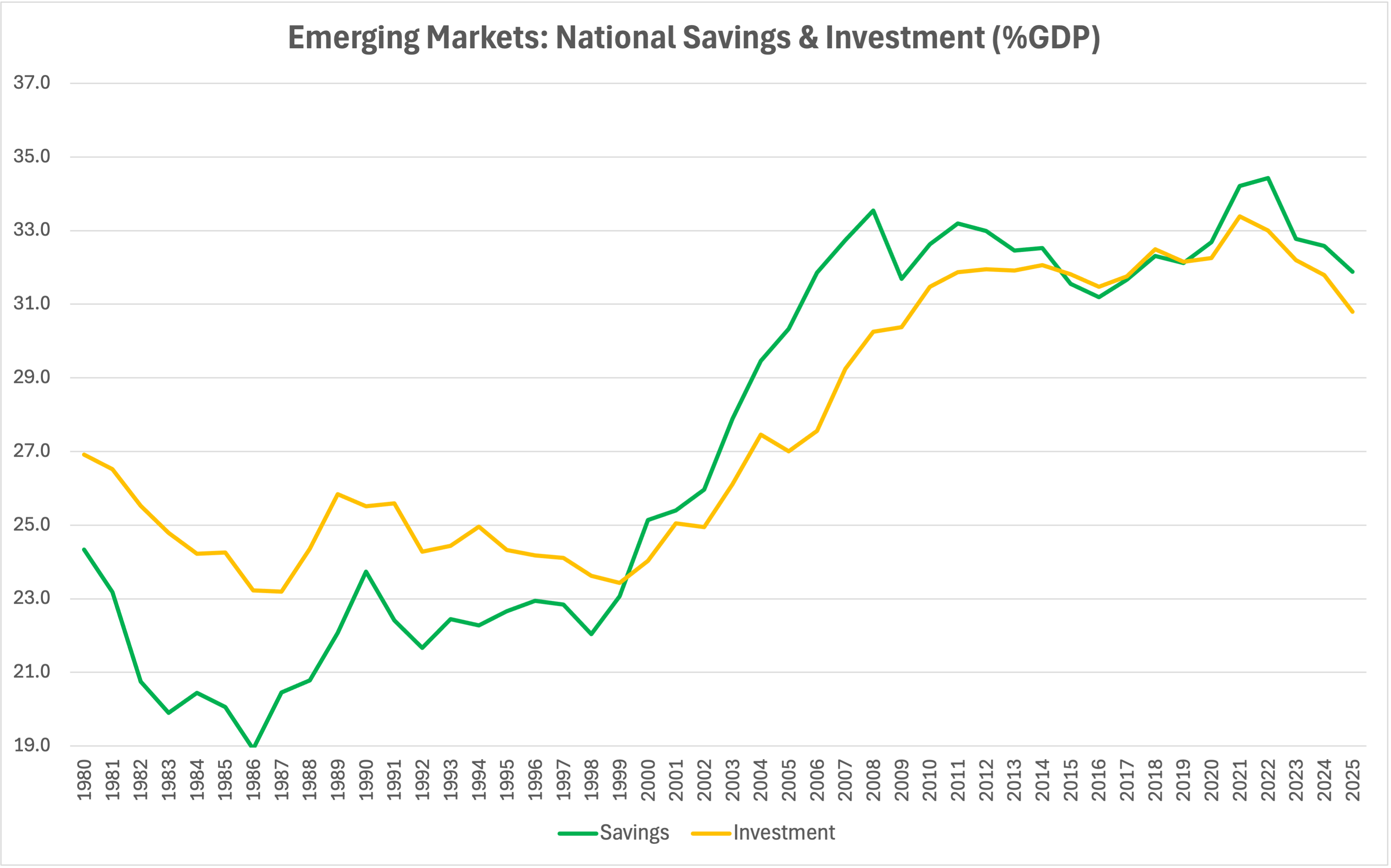

Emerging markets did experience a surge in excess savings between 2001 and 2014, reflecting China’s export boom and stronger revenues for oil producers and other commodity exporters.

One point of clarification before someone rightly raises the red flag. In equilibrium, savings always equal investment. Or rather, for an individual country the difference between savings and investments equals the current account balance — if your savings exceed investment, you’re running a current account surplus. For the global economy, savings must equal investment— it’s an accounting identity. In the IMF data, they don’t because of measurement and coverage issues. In this context, we are really thinking about desired savings and investment at the prevailing interest rate: if desired savings exceed desired investment, the interest rate should fall until the two are equal.

With this caveat in mind, the numbers show at best some suggestive evidence of excess savings starting only in 2001, twenty years after the decline in interest rates began.

Retirement binge

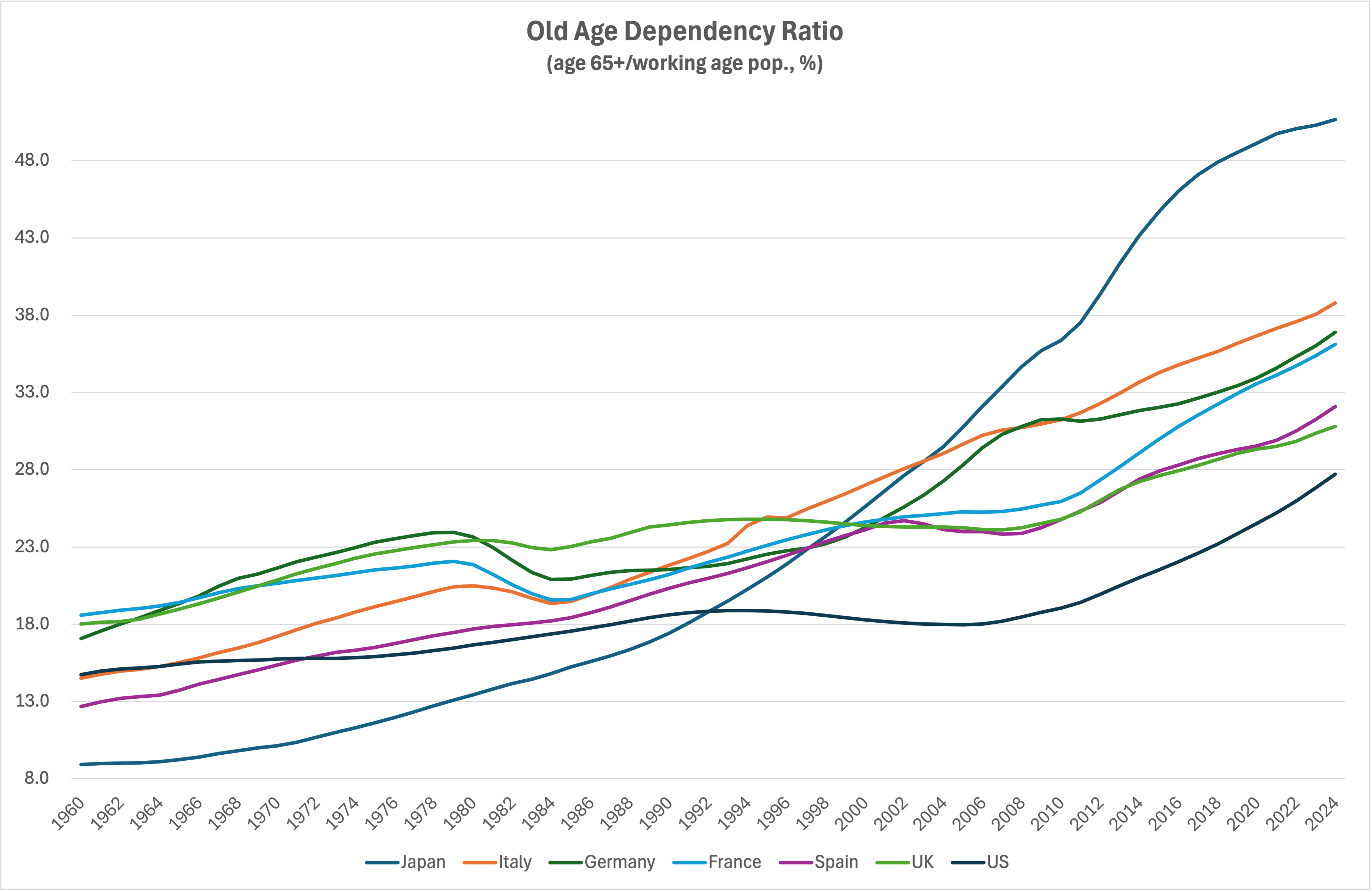

Well, what about those structural drivers of excess savings? There is no doubt that populations in most advanced economies have been aging rapidly. The next chart shows the dependency ratio, i.e., the number of people ages 65 and older divided by the working-age population.

In the early 1960s, all countries in the chart had a dependency ratio below 20%. Today, Japan is over 50%. Italy is close to 40%, Germany and France not far behind. A 50% dependency ratio means every two workers are supporting one retiree. Only the US is still below 30%. And yet…

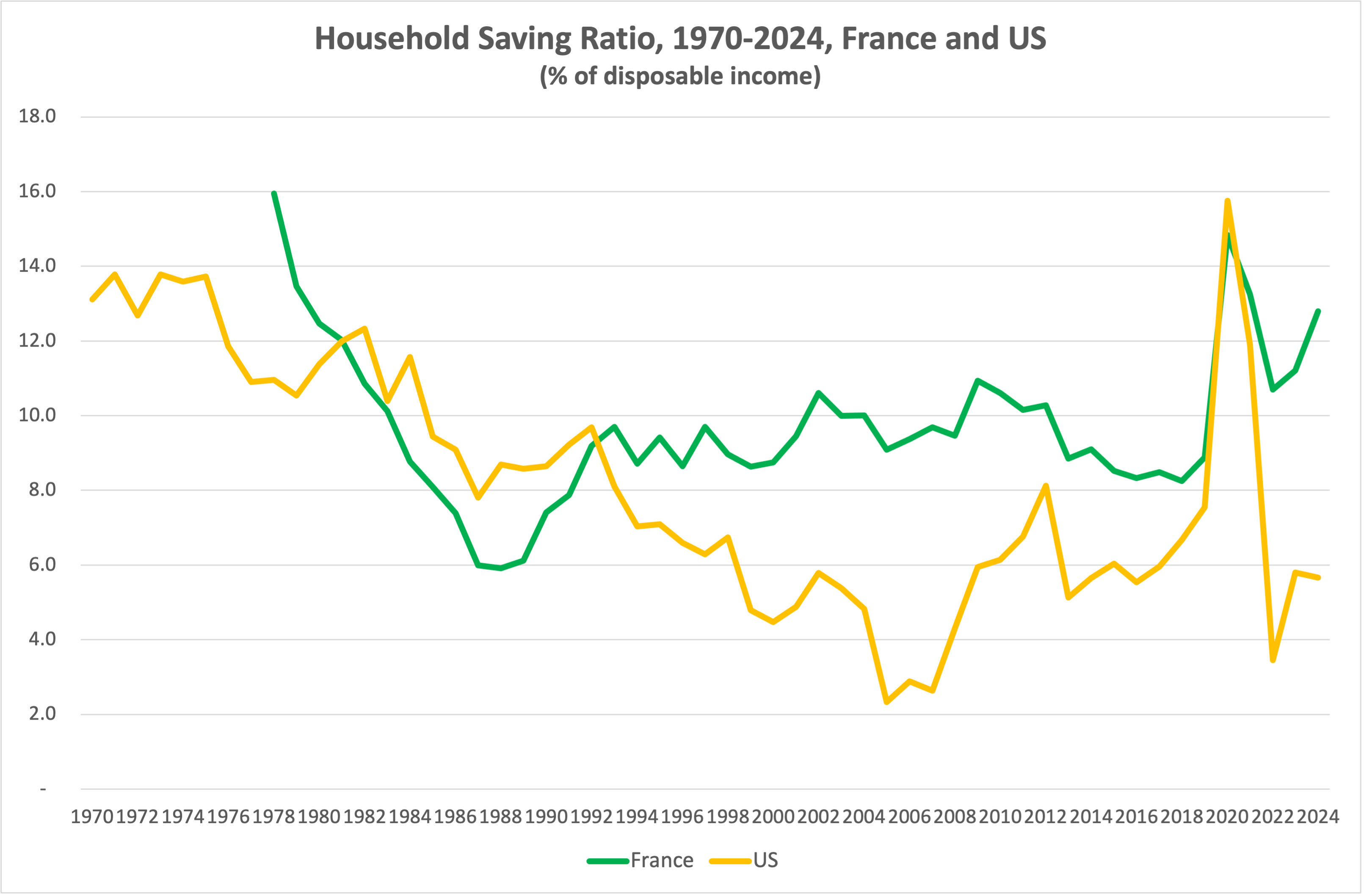

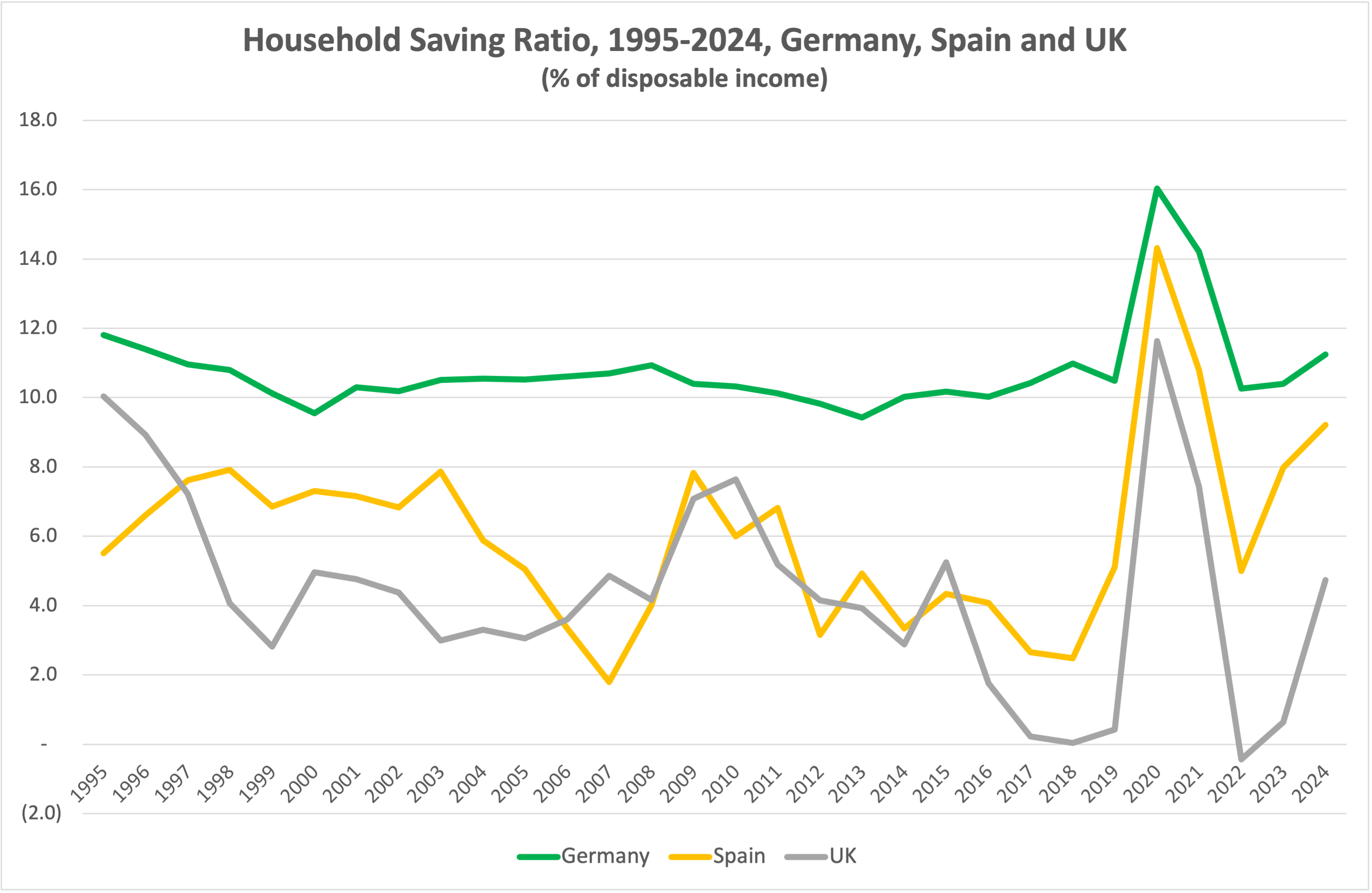

France and the US, for which the OECD has the longest data series, do not show any structural increase in savings whatsoever – though France’s savings remains higher than the pre-pandemic level. Same story for Germany, Spain, and the UK.

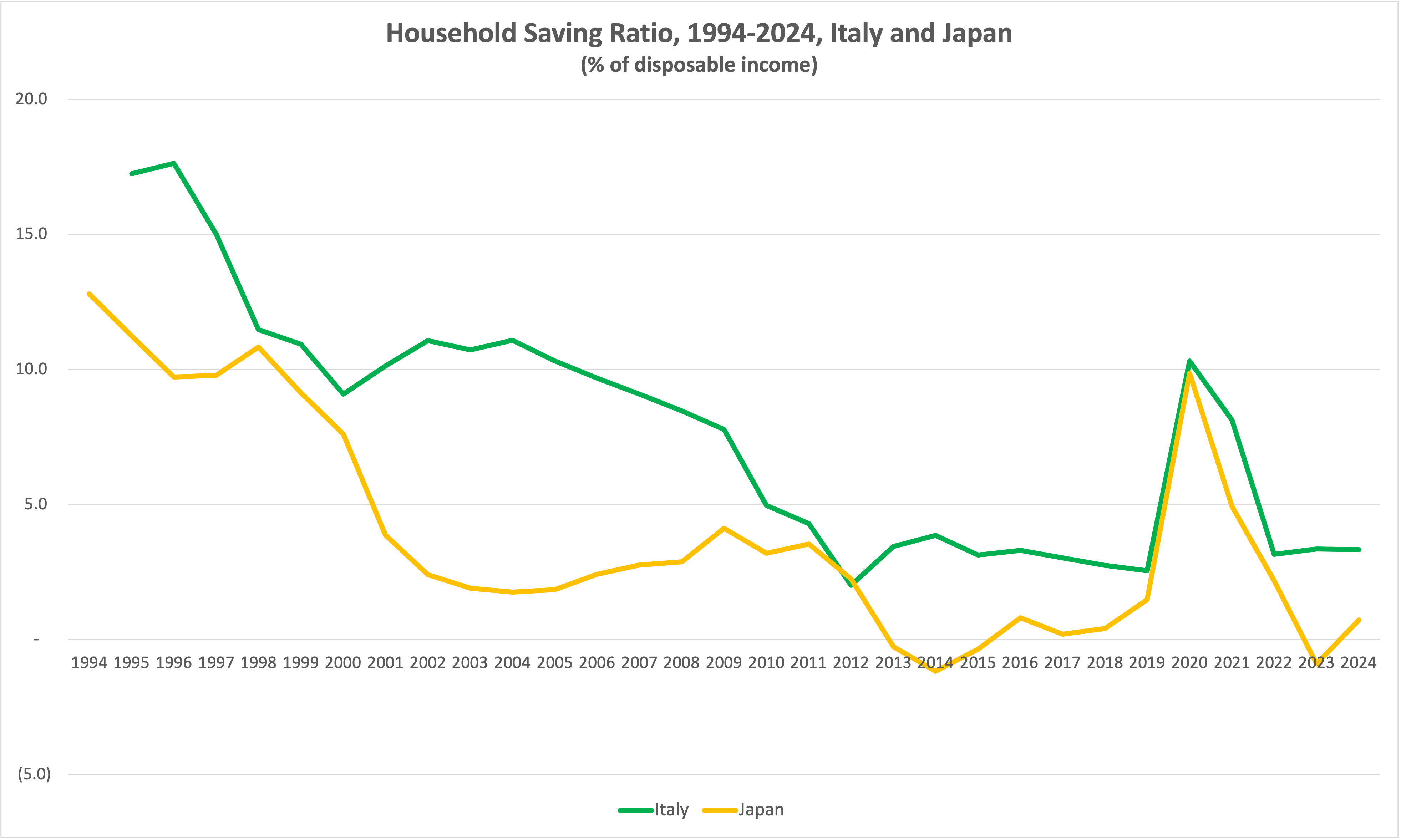

Most striking: in Japan and Italy, the two countries with the worst aging profile, savings rates are five times lower than they were in the mid-90s.

As I wrote in that original post,

Well, there goes that theory.

Longevity has been increasing; populations have been getting older. But household saving ratios have not risen at all. People should be saving more, especially given that pension systems are teetering on the brink of bankruptcy; but they don’t.

This shouldn’t be surprising. The longer your “retired life expectancy”, the more you should save while you are working. Once you retire, however, you will spend, not save — and countries with aging populations have a higher share of retirees

Uncertainty and investment

High uncertainty, as Blanchard noted, is now a feature of the global environment. I would argue this has been true since at least 2007, with the onset of the Global Financial Crisis. But it has had no visible impact on savings, nor has it diminished the appetite for risky investments. The fact is, even in high uncertainty, the need to generate returns eventually takes over — especially if high uncertainty is here to stay.

As for depressed real investment, the energy transition and the AI revolution took care of that. Besides, the need for more real investment is glaringly obvious, not just in emerging markets, but also in advanced economies where legacy infrastructure needs upgrading, and new-generation digital infrastructure needs to be built.

Reality check

The Secular Stagnation theory never stood up to serious scrutiny. Aging populations did not result in higher savings rates, and neither did greater uncertainty. Depressed investment and the rise in hard currency savings by China and commodity exporters proved to be cyclical, not structural.

The crucial driver of low interest rates was the massive, prolonged but unsustainable expansion of monetary policy by the Federal Reserve and other major central banks.

The Secular Stagnation theory, however, was too seductive to be ignored — especially when it counseled governments to spend as much as possible and borrow with abandon. Borrowing, after all, would always be free, and government spending was supposedly the only way to ignite growth. Governments followed the advice: advanced economies debt ratios have surged since the Global Financial Crisis, and governments have become addicted to spending, so that bringing fiscal policy under control is now a daunting challenge.

The rise in interest rates shouldn’t be surprising. What’s surprising is how detached from reality we have become over the past couple of decades. Rising yields are physiological and, so far, unthreatening. We’re crawling back to normalcy. If governments don’t bring fiscal policies under control, however, serious trouble will eventually knock on our doors. The question is how long it will take for governments and for the rest of us to come back to reality.

Don’t follow, subscribe!

I know following sounds easier, less of a commitment. But: Just Think is free and will always be free. I write it because I enjoy writing it and I enjoy the exchange of views with you. Subscribing guarantees you will not miss a timely post. And if you get tired of me, it takes just one click to unsubscribe.