Stagnation Fixation

Secular Stagnation is back from the dead again, claiming that excess saving will forever doom us to low growth and lower interest rates. Nice theory, pity about the facts.

Photo by Quinn Mira on Unsplash

Secular Stagnation has a biblically ominous sound to it. It portends a never-ending future of near-zero economic growth.

It is a zombie theory believed dead in the 1930s but resurrected by Harvard’s Larry Summers in 2013; The surge in inflation of the past two years had put it back to rest, but now MIT’s Olivier Blanchard has brought it back to the forefront.

Save and thou shall stagnate

Secular Stagnation offers a simple explanation for the past fifteen years of low growth, low inflation and low interest rates in advanced economies: we have been saving too much.

Summers argued that excess savings had depressed demand, leading to low growth and low inflation, and pushing interest rates to very low levels. This is the “Stagnation” part. “Secular” refers to the structural causes of excess savings: Summers listed demographics, inequality, accumulation of assets by central banks and sovereign wealth funds, tighter credit standards.

In this view of the world, the equilibrium real rate of interest, the one which would make aggregate demand strong enough to reach full employment, is “sufficiently negative that it cannot be achieved through conventional monetary policy.” Central banks are therefore powerless. Secular Stagnation implies that only governments can save the day: they should spend more, running up debt to stimulate demand.

Interest rates have risen over the past couple of years, but Blanchard has stepped in to argue that they will fall again, because the structural drivers of excess savings are all alive and well:

Demographics, because as populations get older, people tend to save more to provide for a longer retirement;

Higher global uncertainty, which fuels greater demand for safe assets;

Depressed real investment, which will remain too weak to absorb the higher savings — though Blanchard admits greater uncertainty on this point.

The Secular Stagnation hypothesis, however, does not stand up to scrutiny:

Who’s saving who?

Secular stagnation says that excess savings reduce consumption and economic growth and compress interest rates by boosting demand for financial assets. This would make sense in a closed-economy context. But proponents of Secular Stagnation conflate global factors with factors specific to advanced economies.

Both Summers and Blanchard ascribe Secular Stagnation to advanced economies, but Summers recognized the important role of asset purchases by foreign central banks and sovereign wealth funds, which reflect excess savings in emerging markets.

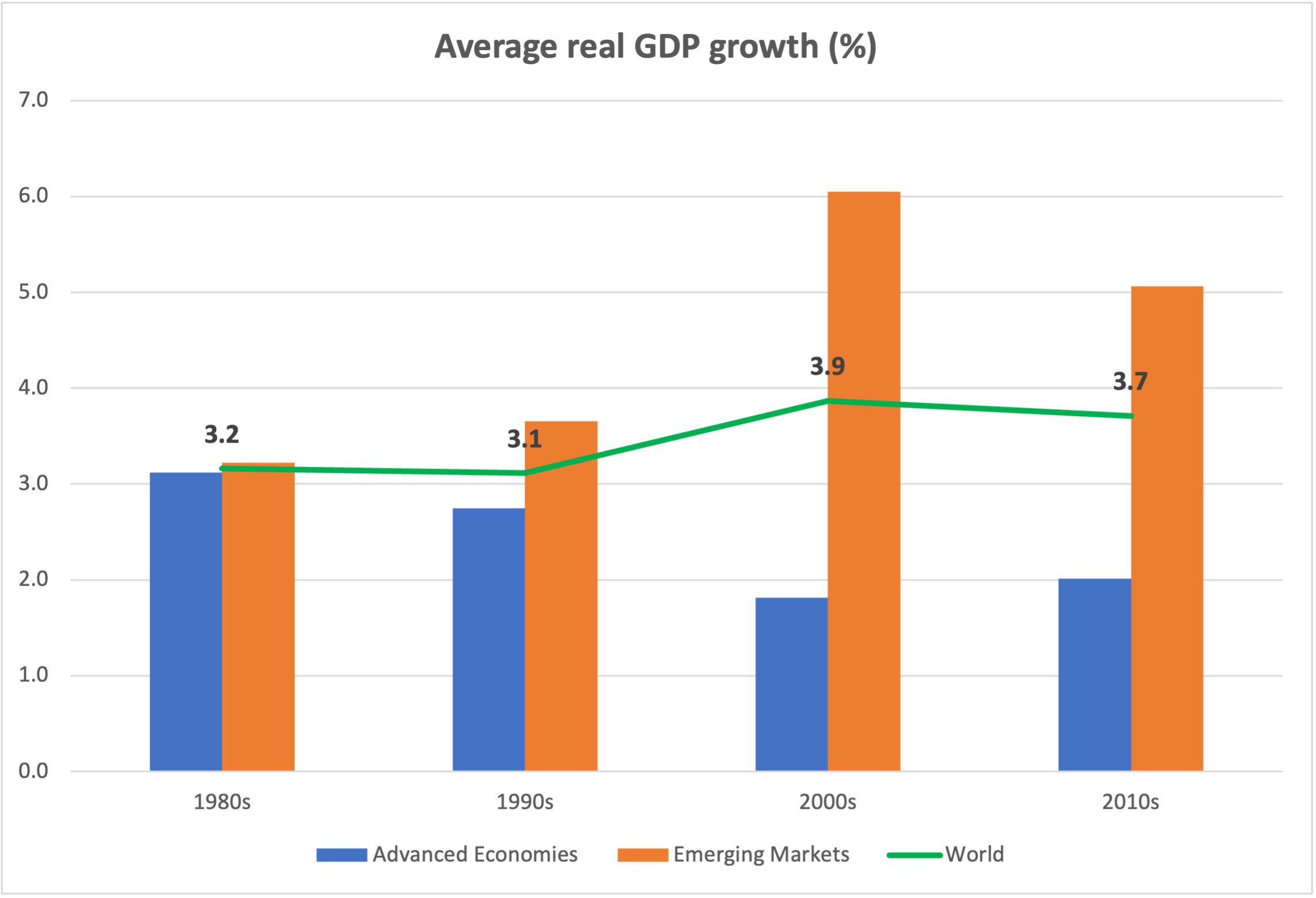

It is only in advanced economies that economic growth has slowed, from about 3% in the 1980s and 1990s to about 2% in the 2000s and 2010s. Global growth instead accelerated from just over 3% per year in the 1980s and 1990s to just under 4% in the 2000s and 2010s, propelled by emerging markets (EM). The global economy did not suffer from secular stagnation. Here is the chart:

Source: IMF, World Economic Outlook

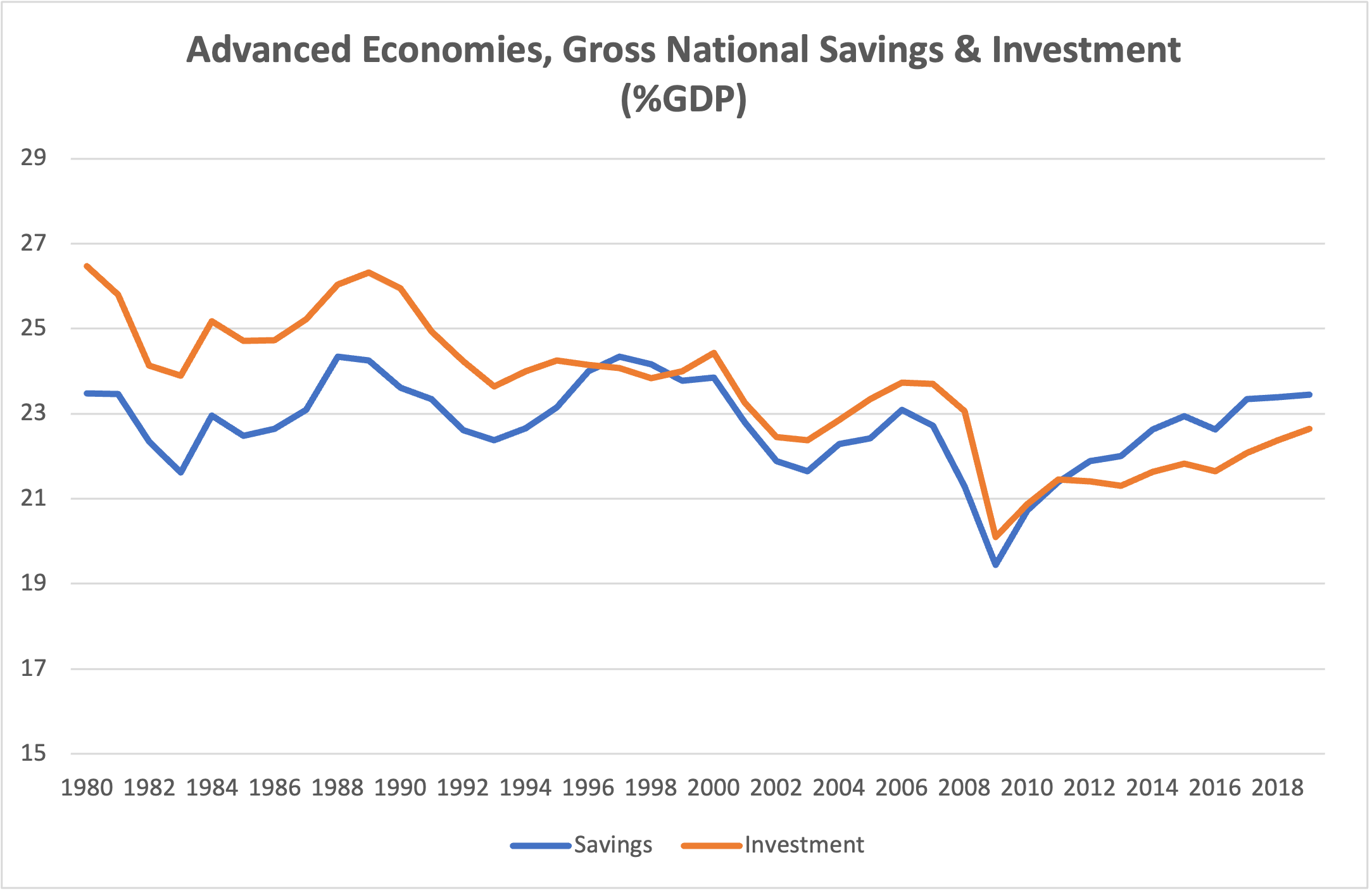

According to Secular Stagnation, it should be excess savings in advanced economies that reduce consumption and growth and depress interest rates.

Let’s take a look:

Source: IMF, World Economic Outlook

Hmm. For most of the 1980-2011 period, investment exceeded savings. An excess of savings appears only from 2012, as investment remained sluggish in the post-GFC recovery; it can’t be responsible for the decline in real interest rates that started in the 1980s or for the growth slowdown which started in the 2000s. I am ending these charts at 2019 because the pandemic artificially boosted savings as people received substantial subsidies and were prevented from partaking in most spending activities; latest US quarterly data show that the saving ratio has already dropped back to historical lows.

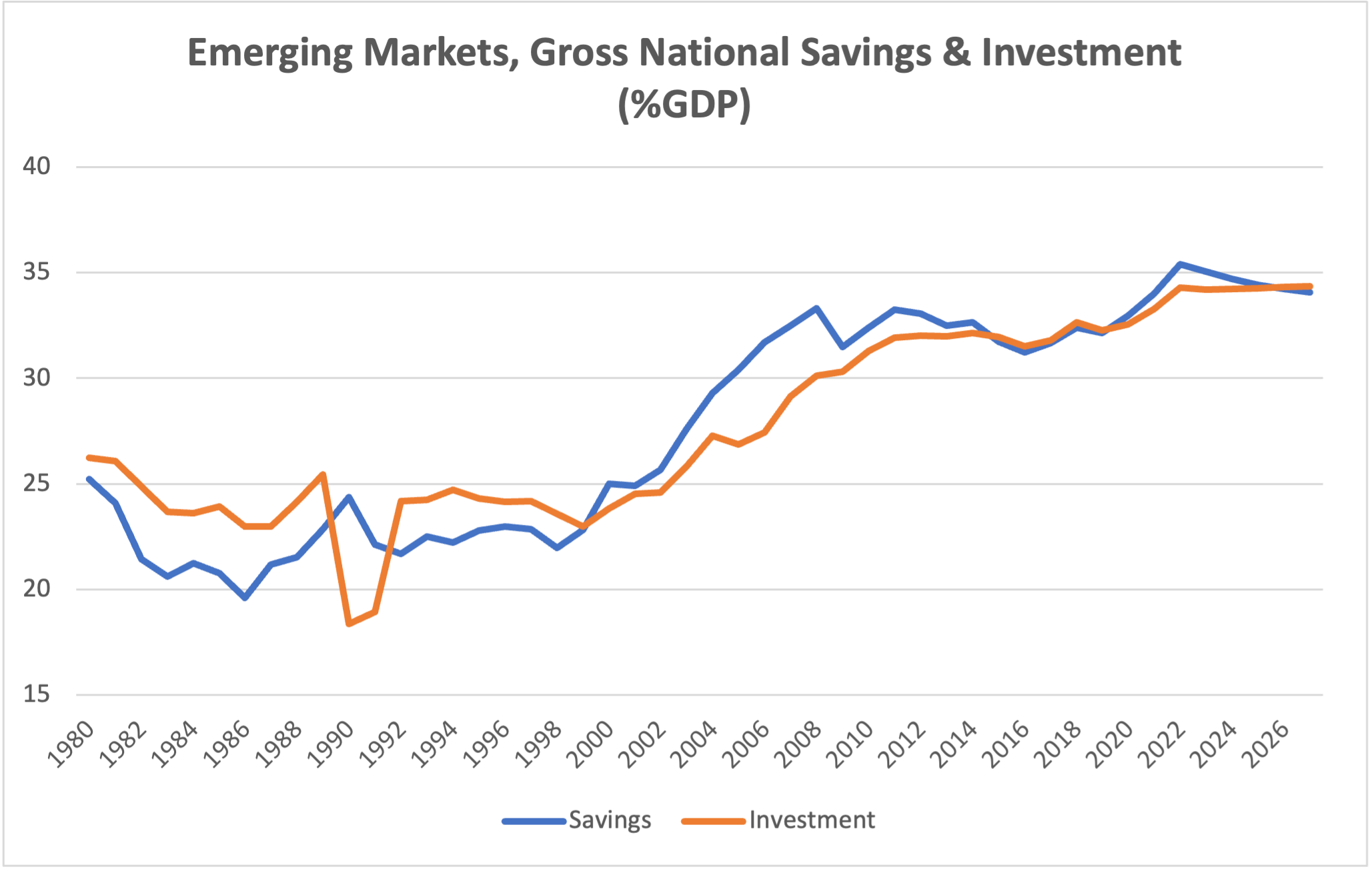

Excess savings in EM did play a role. Between 2001 and 2014, emerging markets experienced a surge in savings in excess of investment, reflecting China’s export boom and buoyant revenues of oil producers and other commodity exporters. A lot of these savings were invested in advanced economies government bonds, especially US Treasuries.

Source: IMF, World Economic Outlook

This surge in emerging markets savings contributed to depress interest rates in advanced economies, but it did not cause slower growth — it was rather a result of the booming EM growth which drove the global economy, supporting advanced economies as well.

Moreover, excess savings in EM are not structural. China’s Current Account surplus averaged over 5% of GDP per year in the ten years prior to 2013, when Summers resurrected the Secular Stagnation theory; in the following ten years it averaged just 1.5% of GDP. Commodity prices surged through mid-2014, then collapsed, then rose again in the last couple of years — and the excess savings of commodity producing countries have gone up and down accordingly.

We should be saving more, but we’re not

This next section is going to be fun.

Demographics are routinely mentioned as the leading structural cause of lower interest rates. Blanchard tells us that as people in advanced economies live longer, they save more to provide for a longer retirement. But do they?

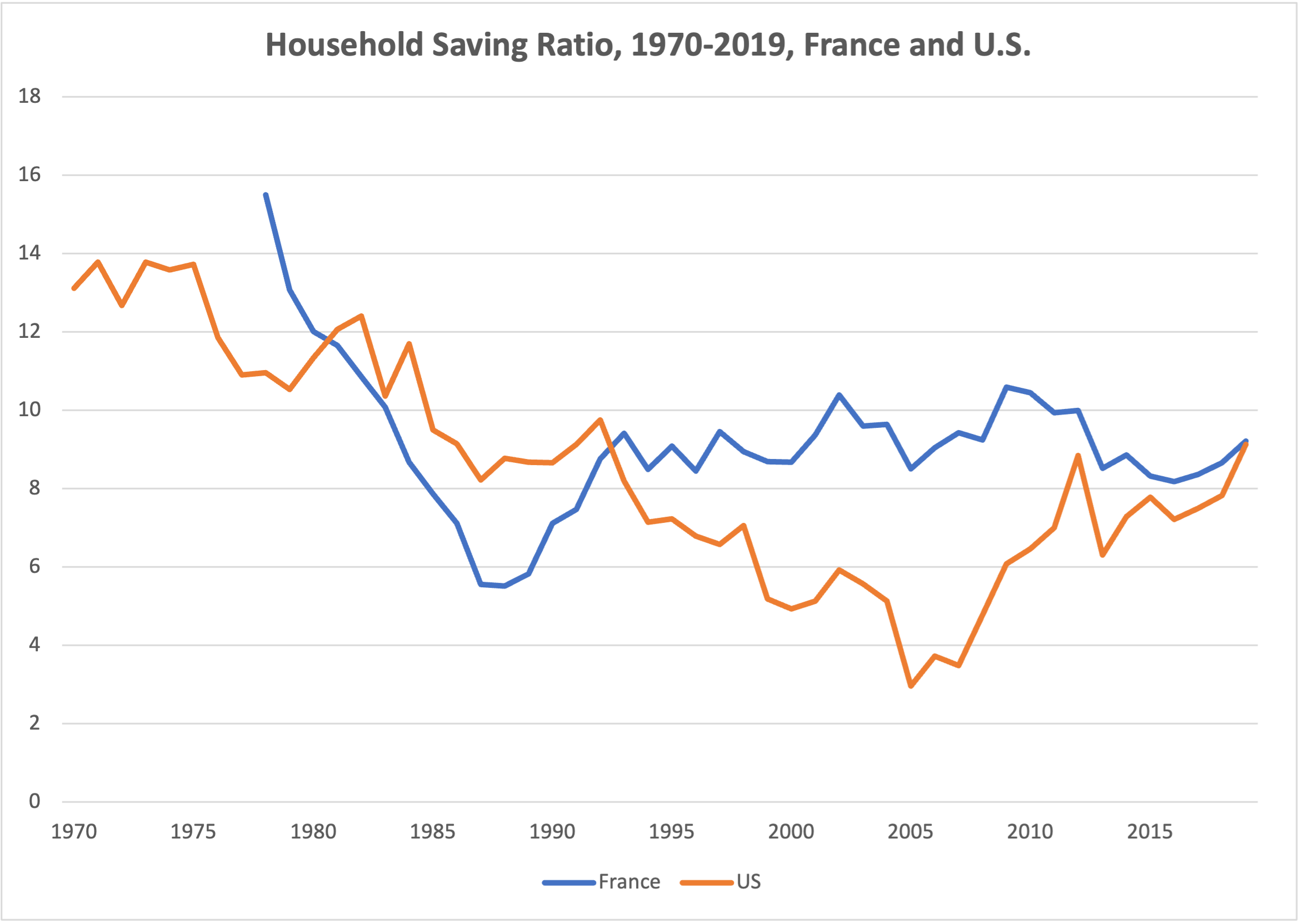

The next three charts plot household savings rates (as a share of disposable income) for a selection of advanced economies. Let’s start with the US and France, which have the longest data series:

Source: OECD

I see no rising trend. US savings experienced a 35-year sharp decline into the GFC and then some recovery, but remain lower than in the 1970s and 1980s. In France, every attempt to nudge up the retirement age triggers a revolution, so longer life expectancy maps one to one into longer retirement. The incentive to save more should be stronger here than anywhere else; but there’s absolutely no sign of a rising trend in savings.

The next chart is even more striking:

Source: OECD

Italy and Japan have notoriously experienced some of the most pronounced population aging trends. And yet their household saving ratios have been declining, not rising. By 2019, saving ratios were 4-5 times lower than in 1995.

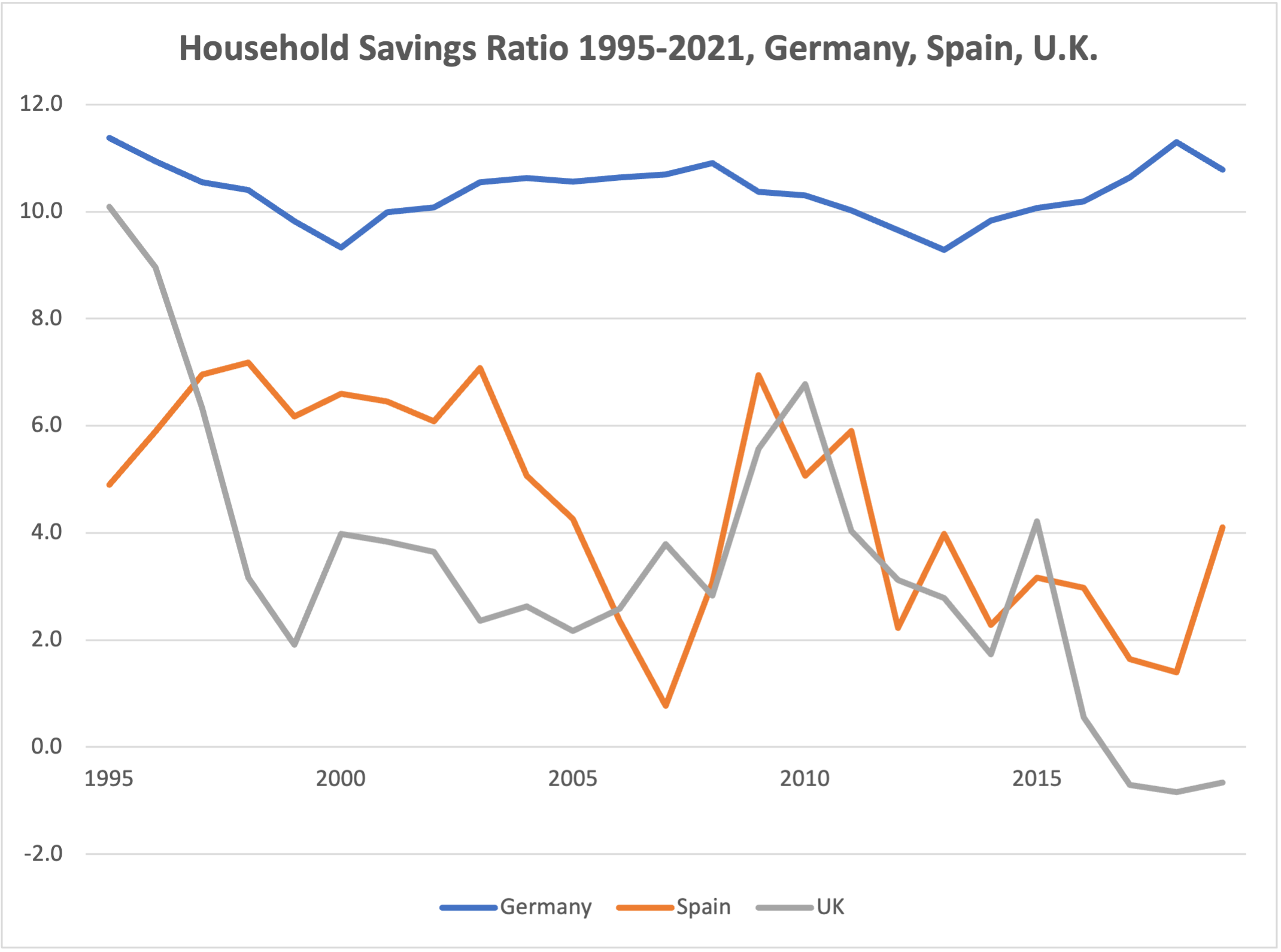

Finally:

Source: OECD

Germany, Spain and the UK do not show any rising trend in savings either.

Well, there goes that theory.

Longevity has been increasing; populations have been getting older. But household saving ratios have not risen at all. People should be saving more, especially given that pension systems are teetering on the brink of bankruptcy; but they don’t.

Incidentally, Manoj Pradhan and Charles Goodhart have argued that population aging has an inflationary effect — the exact opposite of the Secular Stagnation theory. Their reasoning: population aging pushes a higher share of the population into retirement, and therefore contributing to demand — as retirees run down their savings — but not to supply. It seems a lot more persuasive to me.

Uncertainty rises, but so do risky bets

Blanchard argues that greater global uncertainty creates a preference for safe assets. Maybe. But let’s put things in perspective:

In 2008 we had a global financial crisis because too much money around the world had been invested in very risky assets;

Over the past decade we have seen money pouring into crypto assets, non-fungible tokens, and tech companies large and small.

Decades of loose monetary policy and ample liquidity have created massive demand for both safe and risky assets. And with Quantitative Easing, central banks have nearly monopolized the market for safe assets.

To reconnect to the point on demographics: as populations get older, pension funds come under greater pressure to generate the returns needed to pay more pensions. When yields on safe assets are very low, they need to find riskier assets with better returns. We have already seen this over the past decade.

The need to generate sufficient returns eventually trumps the fear of uncertainty.

Nice theory, pity about the facts

According to Secular Stagnation, persistent excess savings have depressed demand in advanced economies, causing weak growth, low inflation and very low interest rates. Excess savings — the theory tells us — are bound to last long into the future because they are driven by structural factors like population aging, uncertainty, and accumulation of assets by foreign central banks and sovereign wealth funds. Therefore, only greater fiscal spending can boost economic growth.

None of this stands up to scrutiny:

Excess savings in advanced economies have only occurred in the last few years, they can’t have caused a growth slowdown starting in the early 2000s, let alone a decline in real interest rates starting in the 1980s.

Demographics, the only truly structural force at play, is a red herring: As longevity increases, people are simply not saving more. Japan and Italy, the countries with the most extreme aging, have seen their saving ratios drop by 4-5x in the last twenty-five years.

Foreign saving have contributed to pushing interest rates down, but some, those of commodity exporters, are cyclical, while China’s have declined to a much lower level — structural, but going in the wrong direction.

Governments have gone on a debt-fueled spending binge as prescribed by the theory, but — as I showed in my last blog — to no avail.

A more plausible explanation is that weak growth in advanced economies is a supply problem, arising from weak productivity growth, higher taxes and pervasive regulations. Meanwhile, safe interest rates have been pushed to very low levels by loose monetary policies, compounded by a temporary strong inflow of emerging markets savings.

Ample liquidity eventually fueled high inflation — in combination with excess demand, again contrary to the Secular Stagnation hypothesis. Central banks are now being forced to tighten monetary policies, pushing interest rates up.

The key implications are the exact opposite of what Secular Stagnation predicts: real interest rates will be higher, population aging will lower labor supply and fuel excess demand, and only supply side reforms and faster productivity can boost economic growth.

If you really still want to hold on to Secular Stagnation, just put a minus sign in front of it, you’ll at least get the right predictions.