Transitory (Dis) Inflation, Growth And Value

Transitory (Dis) Inflation, Growth And Value

There is nothing more foolish than an economist discussing equity markets, but here we go…

The US January inflation report has generated quite a bit of drama in financial markets: equities suffered a large one-day drop — though they recovered ground in the rest of the week — and bond yields rose as investors rushed to scale back expectations of Fed interest rate cuts. At the end of last year, barely over a month ago, financial markets seemed extremely confident that the Fed would start cutting rates in March; now they expect monetary easing to start most likely in June.

Is disinflation transitory…?

Was such a sharp reaction warranted?

Headline CPI did fall, but less than expected. From 3.4% in December it slowed to 3.1% in January compared to consensus expectations of 2.9%. Disappointing, but not dramatically so. More worrying is that core inflation measures remained very elevated. In particular, the supercore measure of services inflation excluding energy and shelter accelerated for the third consecutive month, to 0.9% month-on-month. The six-month annualized rate of supercore inflation is a rather high 5.5%, observes Franklin Templeton's Sonal Desai in her latest blog, where she also notes that shelter inflation might not contribute as much to future disinflation as people expect. The subsequent PPI release confirmed the stronger-than-hoped price pressures, coming in at 0.3% month-on-month for headline and 0.5% for core, against a 0.1% expected for both.

That inflation is proving stubborn should not come as a big surprise given that economic growth continues to show resilience and the labor market remains very tight. Anecdotal evidence and media reports suggest that corporates are becoming more cautious on investment and some are reducing their labor force, but this still looks like a moderate slowdown that leaves in place a robust economic outlook.

On the other hand, there is also no sign at this stage that headline inflation might turn back up. Fed Chairman Powell said at his most recent press conference that he does worry about inflation remaining sticky, but not about a new inflation spike, and the data seem to agree. Overall, the inflation report should have been neither surprising nor shocking.

3-4%: the new 2%?

If inflation stabilizes at 3-4%, how bad is it? Central banks have traditionally targeted 2% on the assumption that higher rates of inflation would prove more volatile. We might be about to find out. If inflation turns out to be as stable at 3-4% as it is at 2%, then we have nothing to worry about. What matters for consumer decisions and business planning is predictability of prices, not the precise rate of inflation.

But the one thing we definitely cannot get with 3-4% inflation is any significant easing of monetary policy. If inflation remains at say around 3%, then a fed funds policy rate of about 5-5.5% might be about right, especially if productivity maintains its recent higher pace of 2% or more.

This has very direct implications for bond yields, so the fact that they repriced higher makes perfect sense if we’re looking at a higher probability of an environment with robust growth, stubborn inflation and therefore elevated short term interest rates.

Value = growth?

But what about equities? (I know, there is nothing more foolish than an economist discussing equity markets. But indulge me, pretend you’re listening to your Uber driver on the way to the airport…).

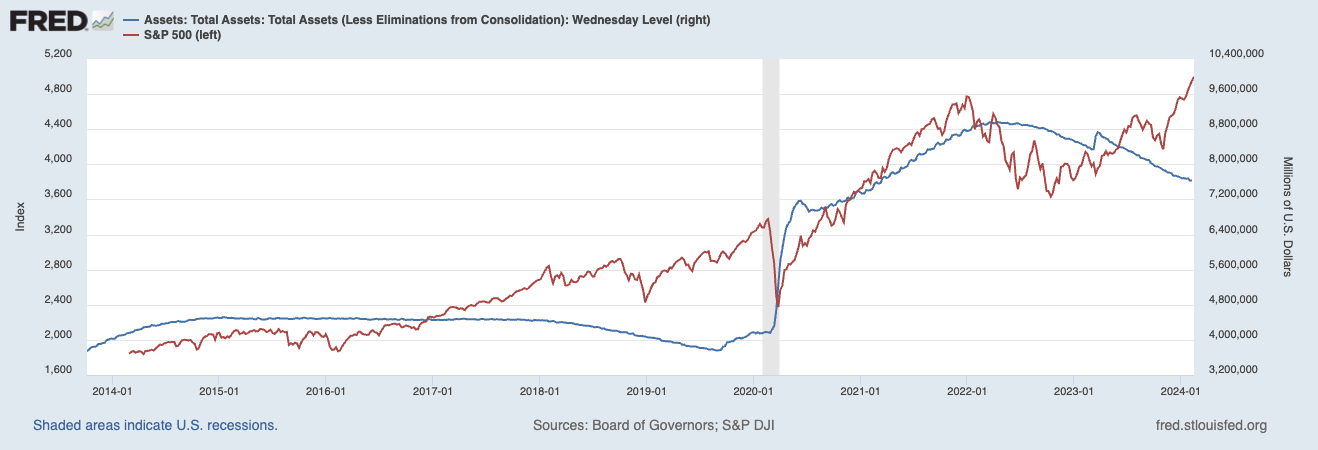

Equity markets are always sensitive to monetary policy moves, for a number of reasons. Interest rates directly affect the discounted present value of future corporate earnings; the stance of monetary policy can impact economic growth and therefore the profitability of companies; and central bank liquidity can directly translate into demand for financial assets. This last factor has been especially important since the Fed launched massive rounds of Quantitative Easing, first to cushion the blow of the Global Financial Crisis and then in response to the pandemic lockdowns. For a while, equity prices seemed to move in lockstep with the Fed’s quantitative easing, as shown for example last year by Apollo’s chief economist Torsten Slok in this post. More recently, however, this correlation seems to have broken: equity prices (S&P 500, in red) have been on a rising trend since late 2022 even as the Fed diligently set to work slowly shrinking its balance sheet.

Fed Balance Sheet vs S&P 500

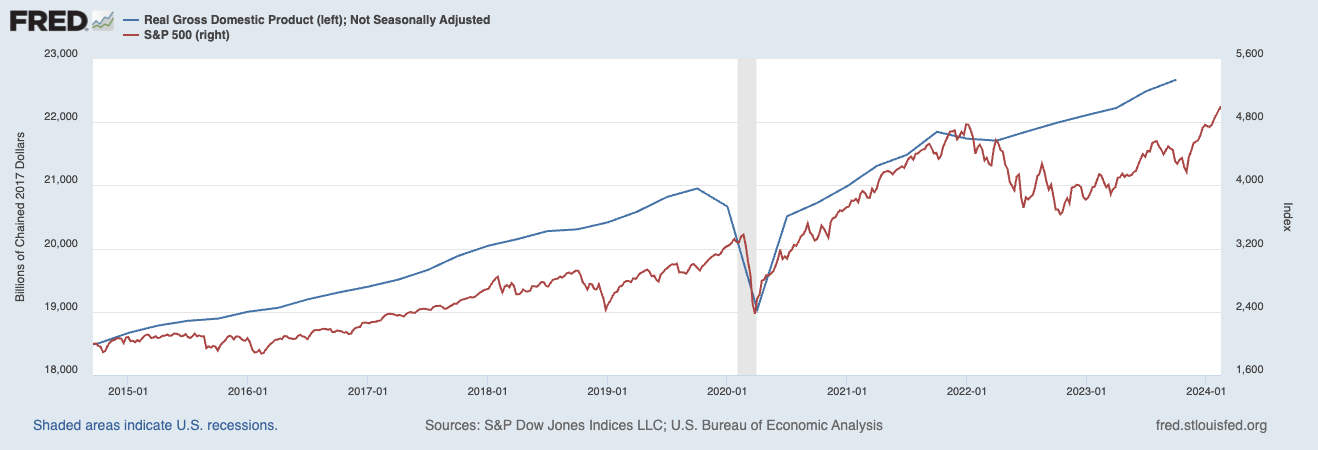

That’s a very good sign. We’d like asset prices — especially equity prices — to reflect the underlying strength of the economy and the profitability of corporate America, not the Fed’s liquidity boosts. Now look at the next chart, which plots the S&P 500 index (still in red) against the level of real US GDP:

US GDP growth vs S&P 500

They trend up together, crash together during the pandemic recession, then recover together. During 2022 however they decouple, with equity prices falling even as the real economy stubbornly keeps rising, defying predictions of an inevitable recession. And 2022 is when the Fed started its monetary tightening, raising interest rates by 4 percentage points over the course of the year.

It looks like investors — long addicted to easy monetary policy — first worried that rising interest rates would spell economic doom, but cheered up when they realized that the economy kept doing just fine. Which to me implies, by the way, that monetary policy is currently not that tight at all.

What about the latest developments? Well, any addiction is hard to shake off, so it stands to reason that hopes of a new “fix” of early and large rate cuts would have boosted markets sentiment. But if the economy keeps growing even with elevated inflation and interest rates, investor sentiment should also recover quickly.

And hopefully over time our collective addiction to easy monetary policy will be cured, or at least alleviated. Then of course we’ll have to worry about our newfound addiction to public debt, but I want to keep this blog upbeat, so let’s not go into that now…