Get A Grip

The Fed isn’t panicking, and neither should we.

Sometimes following economics and markets is just too entertaining. After this week’s Federal Reserve policy meeting, Fed Chairman Powell said quite candidly, we have no clue what’s going on here — and equity markets rallied enthusiastically.

The consensus explanation is rather boring: investors feared the Fed would signal fewer rate cuts, and instead the Fed’s projections still indicated the same two rate cuts as in December. I prefer to think that investors were heartened by Powell’s honesty. Asked why the Fed still envisions two rate cuts even though it now forecasts higher inflation, Powell said something along the lines of, there is so much uncertainty, we really have no idea how we should change our rate forecasts, so we just left them unchanged, out of inertia more than anything else.

Indeed the Summary of Economic Projections shows that FOMC members are a lot more uncertain about inflation, growth and unemployment than they were three months ago. They also see greater downside risks to growth and employment, and greater upside risks to inflation — which is what makes it hard to decide in which direction their rate forecasts might need to be changed.

Who are you going to believe?

Powell is probably frustrated by this policy uncertainty, but he put on a brave face and did not appear too worried. He pointed out that hard data still show healthy economic growth and a healthy labor market. Surveys indicate that consumer sentiment is weakening, but the economy keeps growing — the latest example is a surprising rise in home sales in February. Powell did say “there have been plenty of times where people are saying very downbeat things about the economy and then going out and buying a new car.” That’s a brilliant quote. Who are you going to believe, my data or those flaky survey respondents?

The Fed projected admirable confidence. Eventually policy actions will materialize and clarity will be forthcoming, Powell said, and the Fed is well-positioned to adjust rates as needed. His confidence is not entirely misplaced. Growth is still robust, inflation is not too high, and policy interest rates have been keeping the ship on an even keel, so they’re probably neither way too high nor way too low.

The question, though, is how bad can things get.

No, not tariffs again…

I have talked a lot about tariffs in previous posts and I know you’re thinking, please, not again….

I hear you. Let’s look instead at another issue that has triggered frantic media concern, federal government layoffs. A simple web search pulls up countless sources offering minute-by-minute tallies, maps and charts of government layoffs. Newsweek ominously warns that these personnel cuts “have sparked concerns about economic instability, the strain on unemployment systems, and the disruption of essential government services.”

I’m a small government kind of guy, so you’d have to eliminate the whole government to get me concerned about economic instability and disruption of essential services. Is that what’s happening?

As is customary in our brave new Information Age, finding reliable information is hard. Newsweek talks of “62,530 federal workers dismissed in the first two months of 2025,” and manages to come up with what is probably the most hyperbolic statistic on the topic, saying “That's a dramatic 41,311 percent increase compared to the same period in 2024.” The Associated Press warns that “Potentially hundreds of thousands are affected.” Total federal government employment is about 3 million.

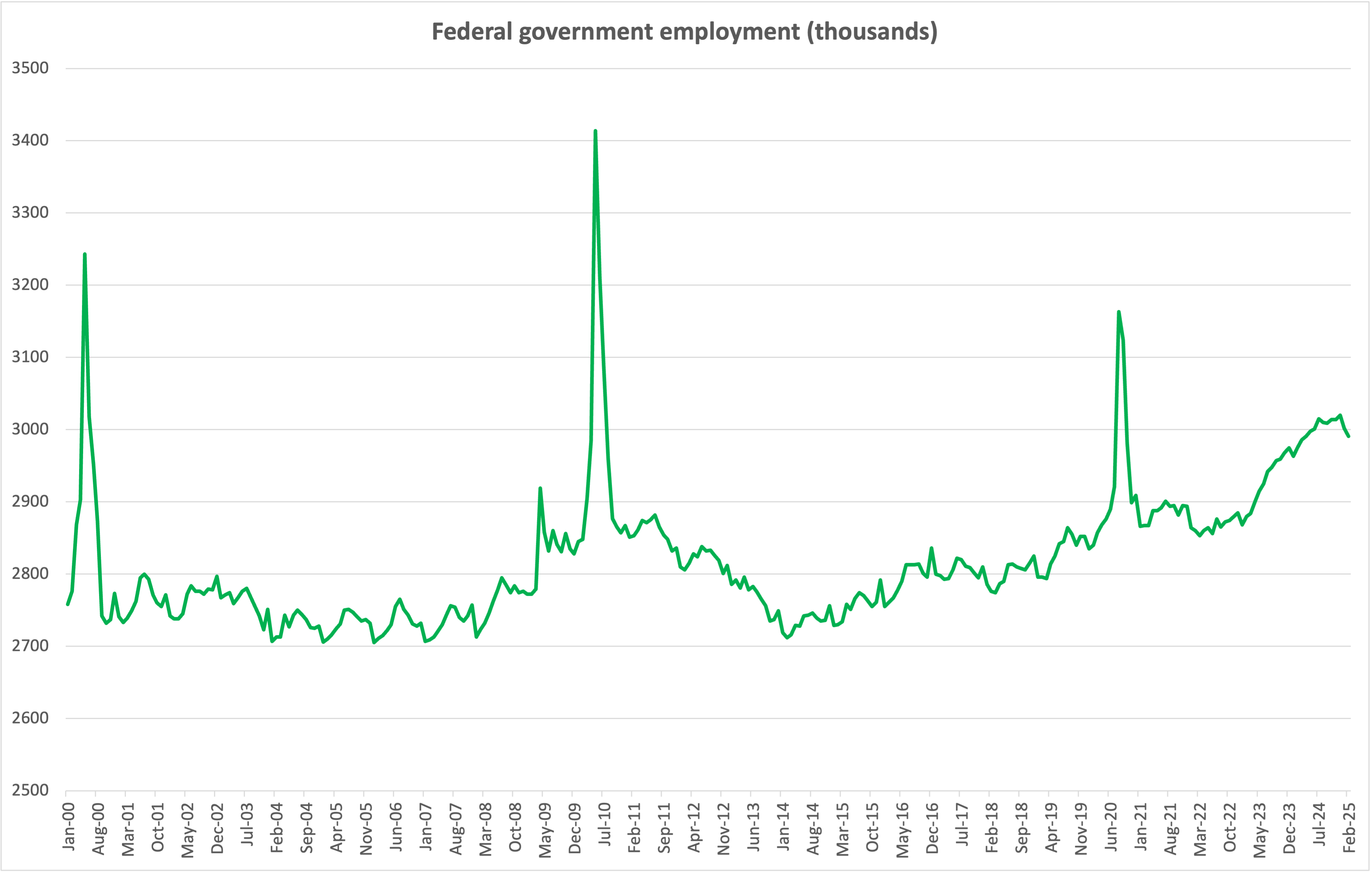

The actual employment numbers show a different picture. Below is a chart of total federal government employment:

Source: US Bureau of Labor Statistics via Saint Louis Fed FRED database.

These numbers show a reduction by 29,000 during January and February. Important, but not in the “hundreds of thousands”.

Moreover, you can see in the chart that federal employment has risen significantly over the past ten years. Ignore the spikes, because those are temporary workers hired to help with the census. Consider the following:

After a surge in 2008-09 and then a decline, by early 2014 federal employment was at about the same level as in the years prior to the global financial crisis. Then over the following ten years it rose by about 300,000 workers, an 11% increase.

Since Trump first came into office in 2017, federal employment is up 6%, or over 180,000 workers.

Of these, 110,000 have been added over the past four years, a 4% increase.

This is a very significant rise in the federal workforce. Raise your hand if you have seen a substantial corresponding improvement in the quality of government services.

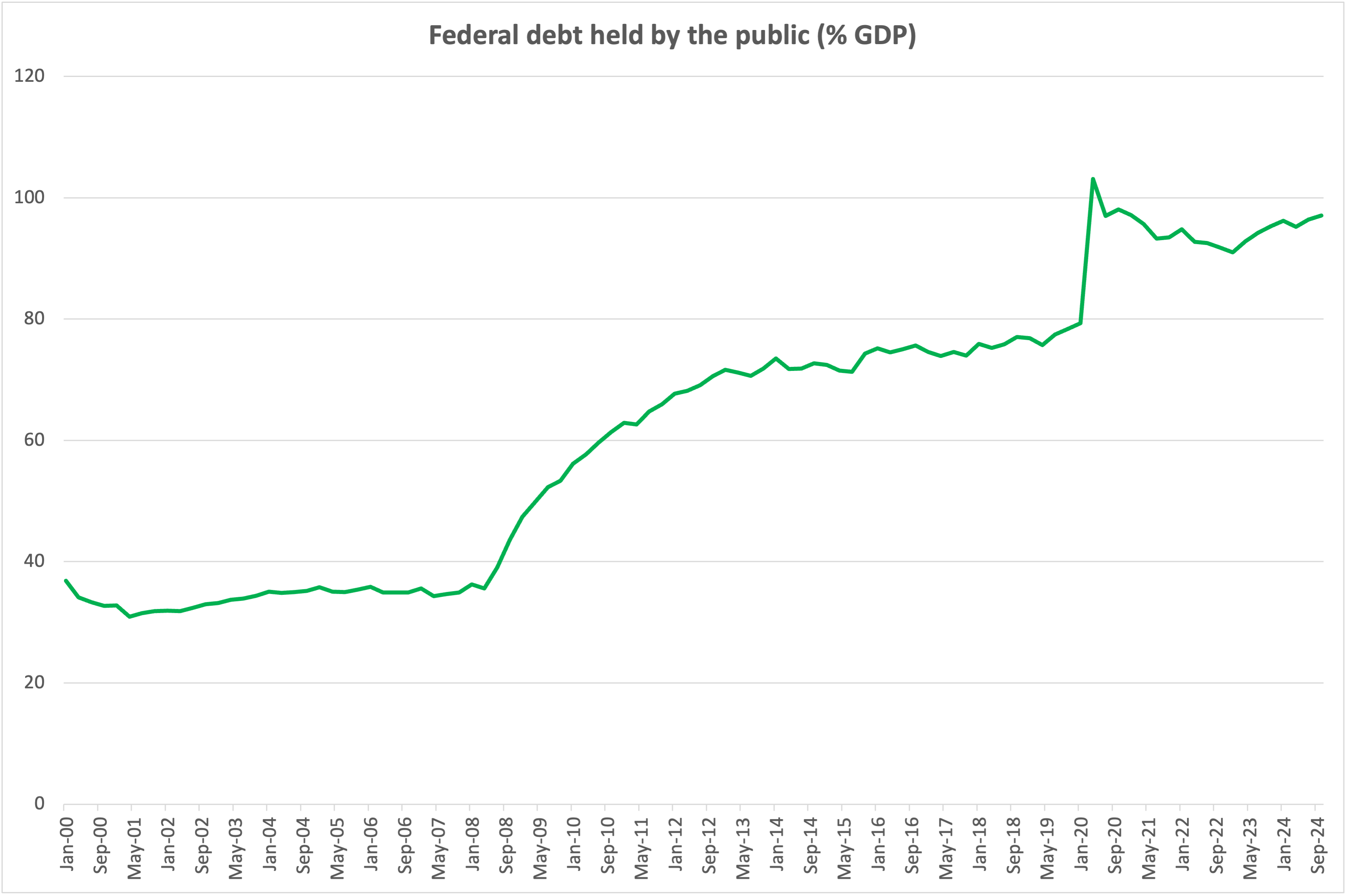

Meanwhile the government’s financial performance has deteriorated, with a sequence of large fiscal deficits that caused federal debt held by the public to triple as a share of GDP since 2007.

Source: US Office of Management and Budget via Saint Louis Fed FRED database.

Get a grip

In a financially underperforming company, a workforce reduction of 5-10% is not unheard of; in fact, it’s par for the course, especially if preceded by significant employment growth.

There are outstanding professionals doing outstanding and important work in our federal government — I know many. There is a risk that layoffs will go too far, that some of the wrong people will be let go, and that there will be some disruption to some services. But we’re not messing with a well-oiled lean and efficient machine here. There is room for improvement. Concerns that public sector layoffs will cause economic instability are way overdone. Which might be another reason why the Federal Reserve is not too concerned yet.

We could all learn from Fed Chairman Powell right now: stop panicking, avoid the partisan hyperboles (on both sides) and keep an eye on the data. The current situation is not great, we knew it going into the election, but it’s not the end of the world. Let’s get a grip.

It’s not about the # of federal employees. The problem with Musk’s & Trump’s vandalism is not that they are reducing head counts, but that they are destroying trust in government (and the average US citizen hasn’t much trust in government to start with). Soon most people may not trust government data anymore, and Trump has already hinted that he thinks there are different types of US Treasury bonds, especially those held by foreigners. It’s not the end of the world, but trying to reduce the immense damage that is done now by Musk & Trump to simplistic head counts of federal employees is a kind of reductionism that doesn’t do it for me.