Between The Dragon And The Eagle

The Western Hemisphere's prospects in a shifting global economy

The original, extended version of this article appeared earlier this week in The International Banker.

President Trump’s administration has escalated trade tensions with Canada and adopted a more forceful stance in Latin America. Against this background, what prospects can we envision for the Western Hemisphere in the global economy?

Over the past three decades, the global economy has undergone a dramatic rebalancing, with the rapid ascent of Emerging Asia. In 1990, China accounted for a mere 2% of the global economy as measured in nominal US-dollar terms; the whole of Emerging Asia barely reached 5%. By 2025, China’s share of global gross domestic product (GDP) had reached 17%, on a par with the European Union (EU). Emerging Asia as a whole reached 24%, closing in on the United States.

The Western Hemisphere held its own. In 1990, the US, Canada, and Latin America and the Caribbean had a combined weight of 34%—a full third—of the global economy. In 2025, their combined share was exactly the same: 34%. The US maintained its 26% share unchanged, Canada shrank by one percentage point to 2%, and Latin America and the Caribbean gained one percentage point to 6%.

This stands in sharp contrast to the European Union, whose share declined by nine percentage points, from 27% to 18%. The Middle East and Central Asia region also lost two percentage points, to 4%.

The Americas’ future role in the global economy will depend on three factors.

The first is the performance of the US. The Iran war casts major uncertainty over the short- and medium-term outlook, but the US economy has demonstrated remarkable resilience over the past years. During 2025, it shrugged off trade-policy uncertainty, a sudden curtailment in labor-force growth, a prolonged government shutdown and attacks on the Fed’s independence. Productivity growth accelerated, and if AI developments fulfill even just a fraction of their promises, this productivity renaissance could be sustained .

The main risk to sustainable US growth, in my view, is unsustainable fiscal policy. Government profligacy has already raised funding costs for corporates and households. And unless the government can streamline public expenditures, getting fiscal policy back on track will sooner or later require meaningful tax hikes, which would again subtract resources from the private sector.

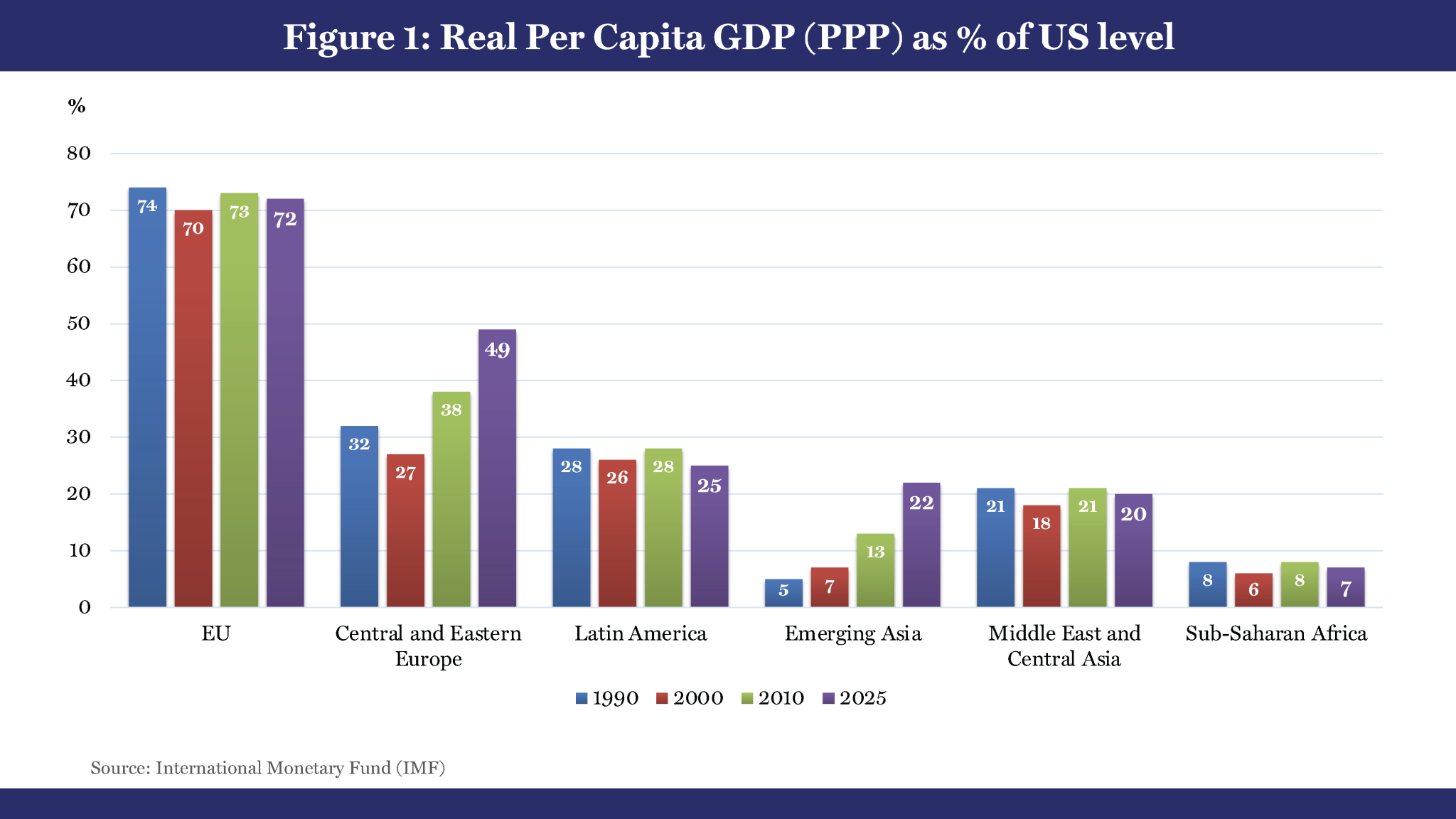

The second factor will be the evolution of economic policies across Latin America. While Latin America has held its share of the global economy, its progress in raising living standards across the region has fallen short. In 1990, average real incomes stood at 28% of US levels. By 2025, they had declined to 25%. By comparison, average incomes in Emerging Asia jumped from 5% to 22% of US levels over the same period and in Emerging Europe from 32% to 49%.

The region’s inability to close the gap with US income levels is rooted in weak productivity growth caused by structural rigidities. The International Monetary Fund (IMF) has estimated that resource misallocation is causing a substantial loss of total factor productivity (TFP), significantly worse than in either Emerging Asia or Emerging Europe. According to the IMF’s assessment, productivity in Latin America is about 40 percent below the levels prevailing in advanced economies. Financing constraints, barriers to competition, regulatory burdens, subsidies and tax distortions stand out as factors that hinder the reallocation of capital and talent to higher-performing firms, making it harder for companies to improve efficiency and achieve scale.

Many countries in the region have oscillated between economic liberalization and government interference. A durable and widespread shift in favor of structural reforms and flexible markets could unleash a productivity boom that would raise living standards and allow Latin America to increase its weight in the global economy.

The third factor will be how Canada and Latin America position themselves in the global trade and supply-chain arena, which the heightened US-China tensions make hard to navigate. Mexico and Canada are the US’ two top trading partners, and the US remains the main trading partner for Latin America overall. China, however, has strengthened its economic presence in the region. It has become the top trading partner for South America. It has launched strategic investments, including in infrastructure, and is aggressively pursuing access to the region’s natural resources.

As I’ve noted in an earlier post, today’s global economy is too deeply interconnected to be split into spheres of influence. Asia’s rapid ascent makes it impossible to ignore. China is the world’s manufacturing juggernaut; it maintains a stranglehold on the processing of most critical materials; and it is investing tremendous financial and human capital into advanced technologies, with impressive results.

Economic relations with China must be approached with caution; but they can be highly beneficial. Canada’s recent shift towards a closer relationship with China acknowledges this. Latin American countries will come under US pressure to be less welcoming to Chinese investment, especially in critical infrastructures and natural resources. But overall, Latin American countries should aim to diversify their trade relations with China, the rest of Asia and Europe. Today Latin American countries are poorly integrated into global supply chains, and their export strategies center mostly on commodities. This needs to change. Bolstering private-sector growth should go hand in hand with seeking deeper, broader integration in global trade flows. This could be simultaneously facilitated by deepening intra-regional trade, which, as the IMF noted, “is between 40 and 50 percent lower than in regions with similar economic and geographical characteristics”.

Abundant natural resources and proximity to the US are huge potential assets. With the right policies, Latin America can leverage them into faster-rising living standards.

The recent emphasis on “spheres of influence” is overblown, in my view, but the economic competition across regions is real. Europe is losing ground, and Asia is advancing fast. The Americas have held their own and have the potential to play a bigger role in the global economy. More constructive relations between the US, Canada and Latin America would help, but it’s national-level policies that will make the difference.

Great piece, Marco. You know that I am less adamant than you about the impossibility of spheres of influence. World War I is a good illustration of how quickly trade and vertically integrated supply chains can unravel under political pressure—particularly foreign policy—which, I would argue, is exactly what is happening today.

In such a scenario—which I concede is still far from the most likely—the turning point towards a more pronounced bipolarity could be the end of Trump’s administration. Let me speculate a bit.

I feel that, by being more proactive and aggressive, Trump’s foreign policy may actually be easier for China to manage than a US with a softer stance. Although it may seem that actions in Venezuela and Iran are setbacks for China (and they might well be), I am not convinced they are causing significant damage. China’s relative silence following these events may reflect a view that, in the current phase of international relations, it can gain favor with countries that feel sidelined by the Trump administration.

You have mentioned Canada, but I would also include the European Union (slow, as usual, but moving in that direction) and possibly India. On India, you may have a different view. But as you noted in one of your previous columns, India has historically not been a natural ally of the US. Recently, in an effort to align more closely, it yielded to US pressure and ceased imports of discounted Russian oil, redirecting demand to the Middle East. Now, with the Strait of Hormuz effectively disrupted, around 30 Indian oil tankers are reportedly stranded, waiting for passage. Just two days ago, two Indian LNG tankers managed to transit thanks to direct diplomatic engagement with Iran’s remaining leadership. At some point, India may feel that the costs of alignment are too high and adopt a more pragmatic stance in balancing relations between China and the US.

If no major conflict breaks out beforehand, the end of Trump’s administration could lead to a return to a softer US diplomatic posture. However, the difficulty the US may face in rebuilding trust with its allies could present a significant opportunity for China to act more proactively and consolidate its influence.

As I said, it's all speculation, but we have experienced a bipolar world before, and there is no reason why international relations should not evolve into a new one.

Regarding Latin America, well... it's somewhat like the eternal promise of Africa's economic surge.

In short: a century of Latin America alignment with US-led and IMF policy frameworks resulted in underdevelopment and 35 years of stagnation (in relative terms). Now that China strengthened its economic presence in the region launching strategic investments, including in infrastructure, meaningful development is finally possible!

Halleluyah! ;-)