An Economist's Thanksgiving

An Economist's Thanksgiving

Economists of widely different views are all lining up to say, "we were right"! I bring them to you for entertaining Thanksgiving dinner banter, and I'm thankful to be in their blessed number.

Photos by Luke Chesser and Suzy Brooks on Unsplash

Economists: let’s face it, we haven’t covered ourselves in glory in the last…at least thirty years?

We saluted the Great Moderation (no more recessions! We’ve defeated the economic cycle!) while we sowed the seeds of the Great Financial Crisis;

Then we promptly panicked about a new great depression and inevitable deflation, responding with reckless policy easing;

We blessed a global economic shutdown for a virus that now turns out to have had a fatality rate for the non-elderly comparable to the flu (0.0.3% for ages 0-59 and 0.06% for 0-69), while those who advocated a targeted protection (April 2020 here and more famously October 2020 here) were treated like criminals;

We compensated with an even more reckless policy easing, because anyway…

… we had claimed inflation was dead for good, never to be seen again…

…and were promptly rewarded with the highest inflation rates in half a century.

I could go on, but you get the gist. So it is a bit funny to see different gangs of economists line up in the papers and social media to claim “we were right” and “we told you so.”

I offer you some examples that could make for entertaining conversation around the Thanksgiving table — less exasperating and depressing than arguing about politics.

Transitory Victory Laps

My favorite example is Team Transitory, the economists who when inflation spiked assured us it was a passing disturbance entirely due to exogenous shocks that would quickly disappear with no need for policy intervention (Covid disruptions to supply chains plus the energy price increase from the Ukraine war). Now that inflation has finally climbed down to less frightening levels, they claim they were right all along, there was no need for the rest of us to get all excited nor for the Federal Reserve to tighten policy.

In their view, the fact that inflation declined while growth remained resilient proves that inflation was entirely due to temporary supply problems that have now faded; rate hikes contributed nothing to the inflation decline, but, however, should definitely be blamed if the economy falls into recession. Prominent voices here include Paul Krugman and Joe Stiglitz, the latter with an article titled…A Victory Lap for the Transitory Inflation Team. I kid you not.

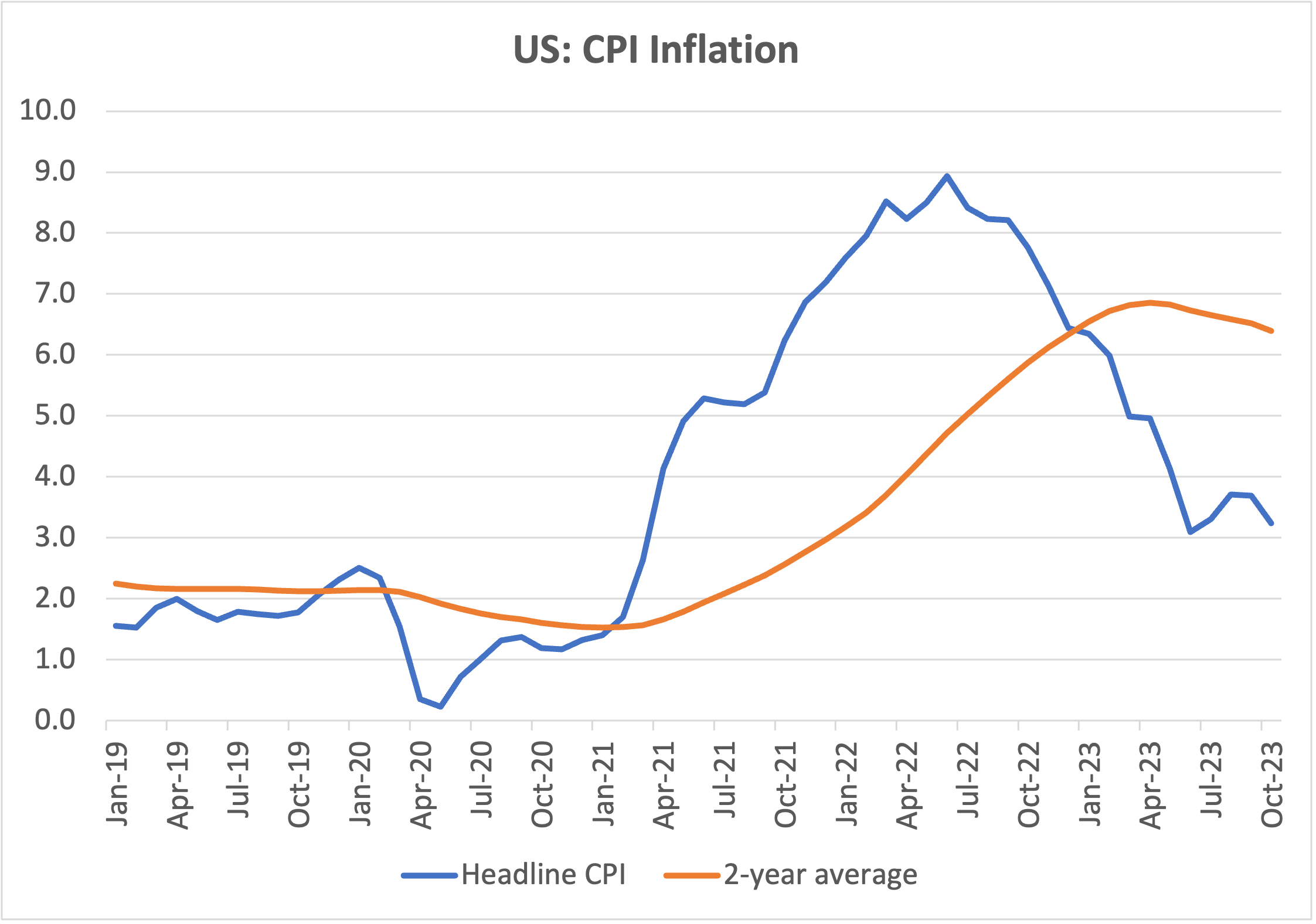

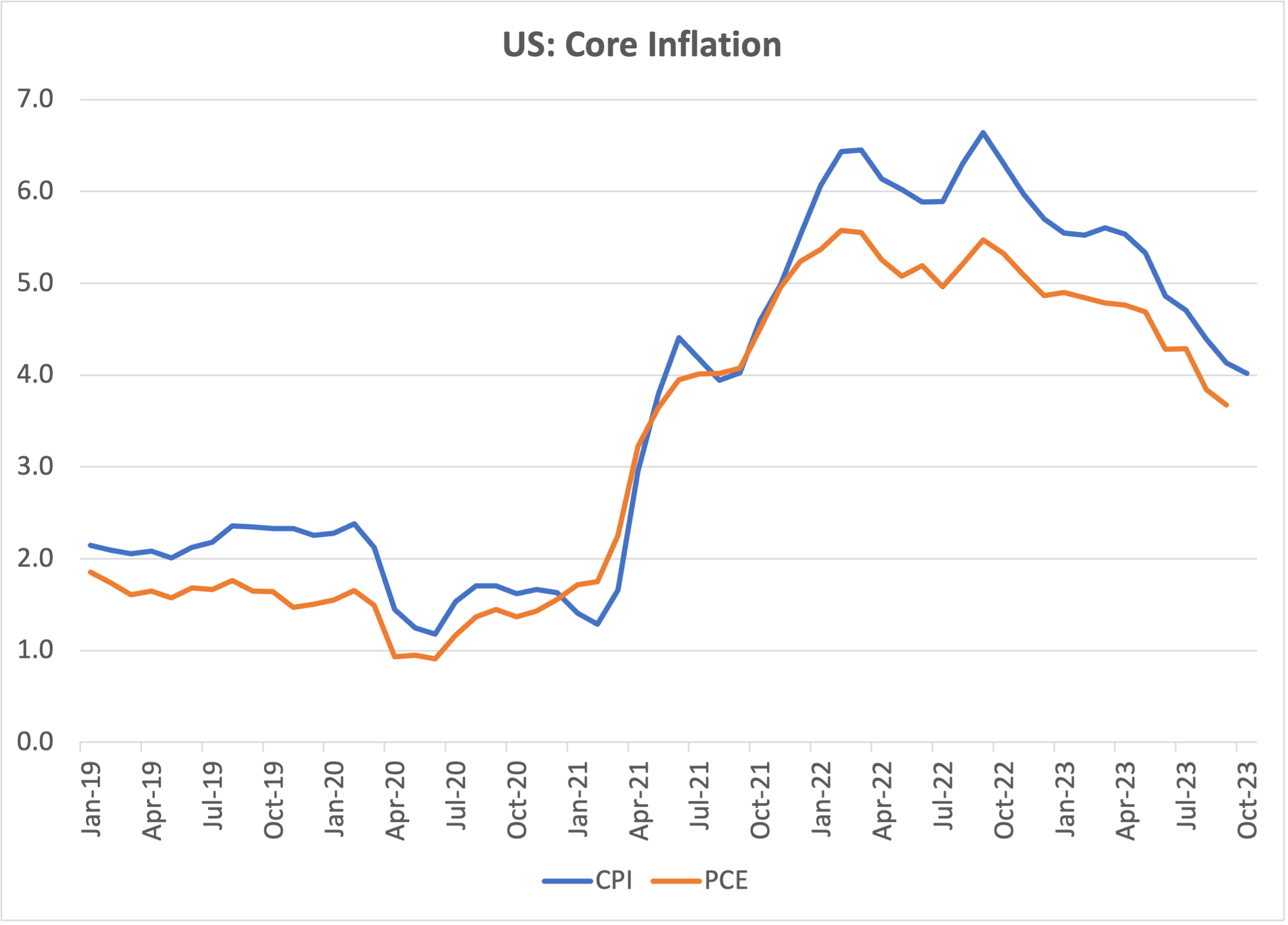

They conveniently ignore that demand has weakened as higher rates made mortgages and credit more expensive, and it’s hard to believe this had no impact on price dynamics. They also ignore that decisive rate hikes were probably instrumental in keeping inflation expectations under control, which again helped bring inflation down. Most importantly, inflation averaged over 6% for the last two and a half years. Two and a half years! This is not at all what team transitory meant by "transitory", so they're really shifting the goal posts here. I guess since nothing is eternal, everything can be called transitory. Let’s look at it this way: even with very sharp monetary tightening, headline CPI averaged over 6% for two and a half years and core inflation is still at 4% — it seems bizarre for team transitory to take a victory lap.

Source: US Bureau of Labor Statistics

At the other end of the spectrum, some economists who correctly predicted the persistence of high inflation are now tempted to minimize the disinflation achieved so far, and some seem to even gleefully anticipate a new inflationary shock — turmoil in the Middle East and the ongoing war in Ukraine are often mentioned. To be fair, the more thoughtful among them always conceded that exogenous shocks had played an important role and that getting inflation down from 9-10% to 4-5% would be relatively easy. They also maintained the last leg down to the 2% target would be much harder, and it might well prove to be. Bottomline, they can also say, “we were right!”

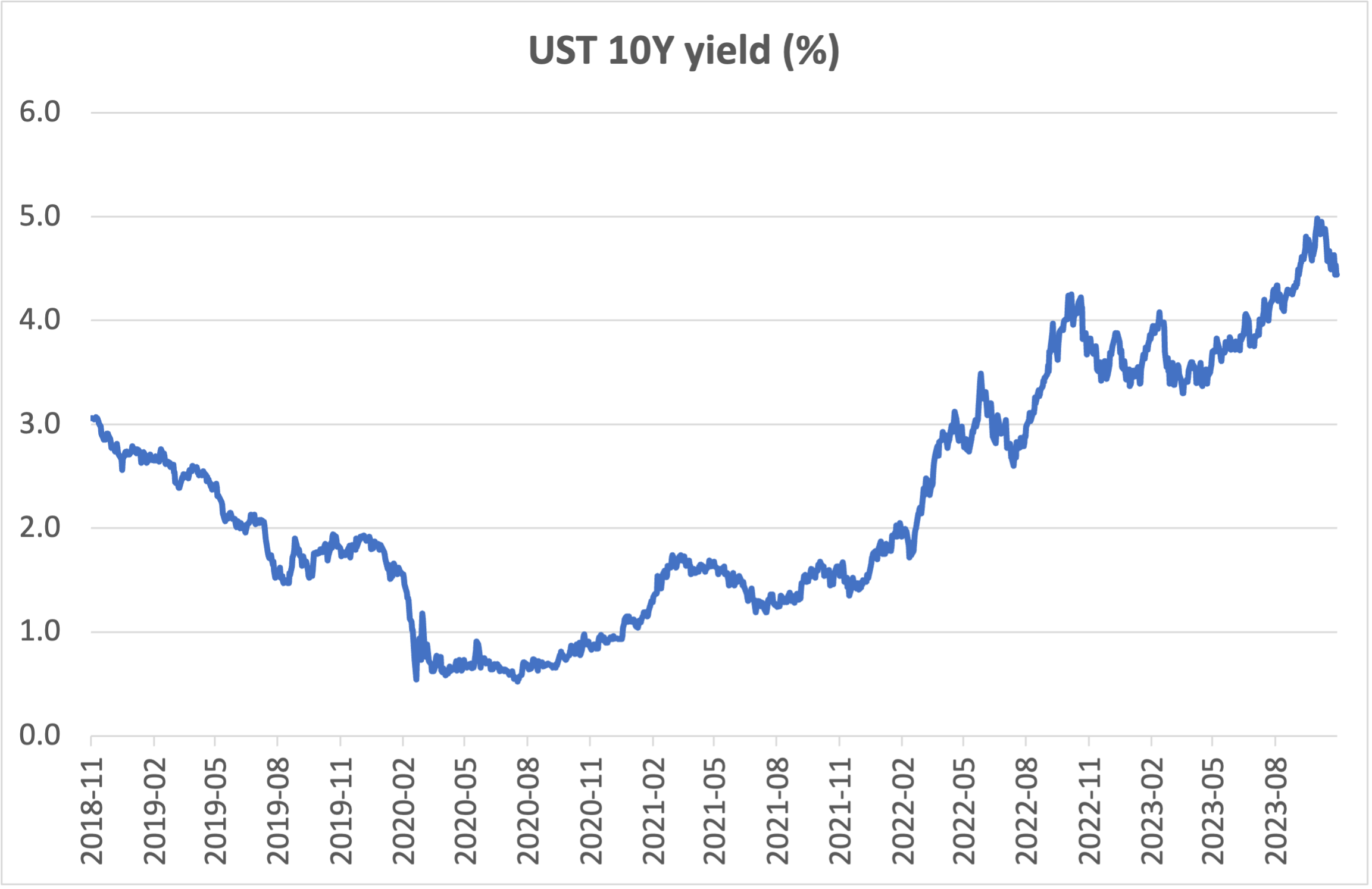

Both camps have made themselves hostage to the vagaries and whiplashes of the fixed income market: as yields on 10-year US Treasuries jump up and down, one set of economists claims victory while the other sulks; a week later the roles are reversed, then reversed again… This is even more entertaining if you, like me, believe that swings in bond yields are driven a lot more by the waxing and waning of hopes for looser monetary policy than by any assessment of underlying economic trends.

Source: Board of Governors of the Federal Reserve System

Modern Monetary Turkey

Then there are the prophets of Modern Monetary Theory, which holds that a government that prints its own currency does not have a budget constraint and can spend with no limits (Argentina’s new President Javier Milei, who wants to adopt the US dollar, clearly did not get the memo). You and I might be concerned by the skyrocketing US public debt, which contributed to the inflation spike and to dangerous volatility in the US Treasury market, and will be a headache for the US economy for years to come. But the MMT crowd see it as something that helped the US economy remain robust, with no adverse consequences. They, too, were right all along!

Happy Thanksgiving

So this Thanksgiving I will give thanks for being an economist, part of a select community of people blessed with the ability to believe that we were always right, regardless of where the wind of reality might blow - and even before Artificial Intelligence starts generating different customized realities for every one of us…

So instead of arguing over politics, have a good laugh at our expense.

Happy Thanksgiving!

Very droll Marco!😀