Voodoo Economics

Voodoo Economics

The Fed, markets, and the struggle for economic sanity.

Listening to this week’s Fed press conference after the momentous 50 basis points rate cut I found myself wondering, wait, why do we need looser monetary policy? Fed Chairman Powell spent the bulk of his time telling us that the US economy is strong, and the labor market is at full employment, just inching away from an extremely overheated state.

An odd way to justify a 50bps rate cut. Powell’s problem, however, was that too many analysts and investors seemed convinced a recession is just around the corner. Since the Fed was known to be choosing whether to reduce rates by 25 or 50bps, the larger cut might have signaled concern about the growth outlook. So Powell had to reassure investors on the strength of the US economy. It wasn’t that hard: with the latest encouraging retail sales and the August rebound in industrial production, GDP growth estimates for Q3 sit in 2.5-3% range. And at 4.2%, the unemployment rate is still extremely low and the labor market at full employment — even after absorbing an important boost in the labor force partly driven by immigration.

the unthinking invocation of mysterious magical empirical regularities

Voodoo economics

So why would anyone be worried about a recession? Blame the poor state of economic analysis these days: too often we hear arguments that sound like the equivalent of technical analysis in financial markets — the unthinking invocation of mysterious magical empirical regularities. In technical analysis they sound something like “whenever the 7-day moving average of company’s X stock price breaches its 194-day resistance level, it invariably breaks upwards with an average gain of 8.3% over the subsequent ten trading days.” Ask why, and you will be met with blank stares: it just is, the visible manifestation of immutable laws that our limited minds cannot yet comprehend.

In economics this takes the form of things like the Sahm rule: “when the three-month average U.S. unemployment rate rises by 0.50% or more from its 12-month low, a recession is underway.” Or the law according to which an inversion of the yield curve (short-term interest rates higher than long-term interest rates) always predicts a recession in the near future. Except that the Sahm rule was triggered nearly two months ago, and the US economy powers ahead unperturbed. And the yield curve had been inverted for about two years starting in the summer of 2022, and again the US economy did not get the message and kept expanding.

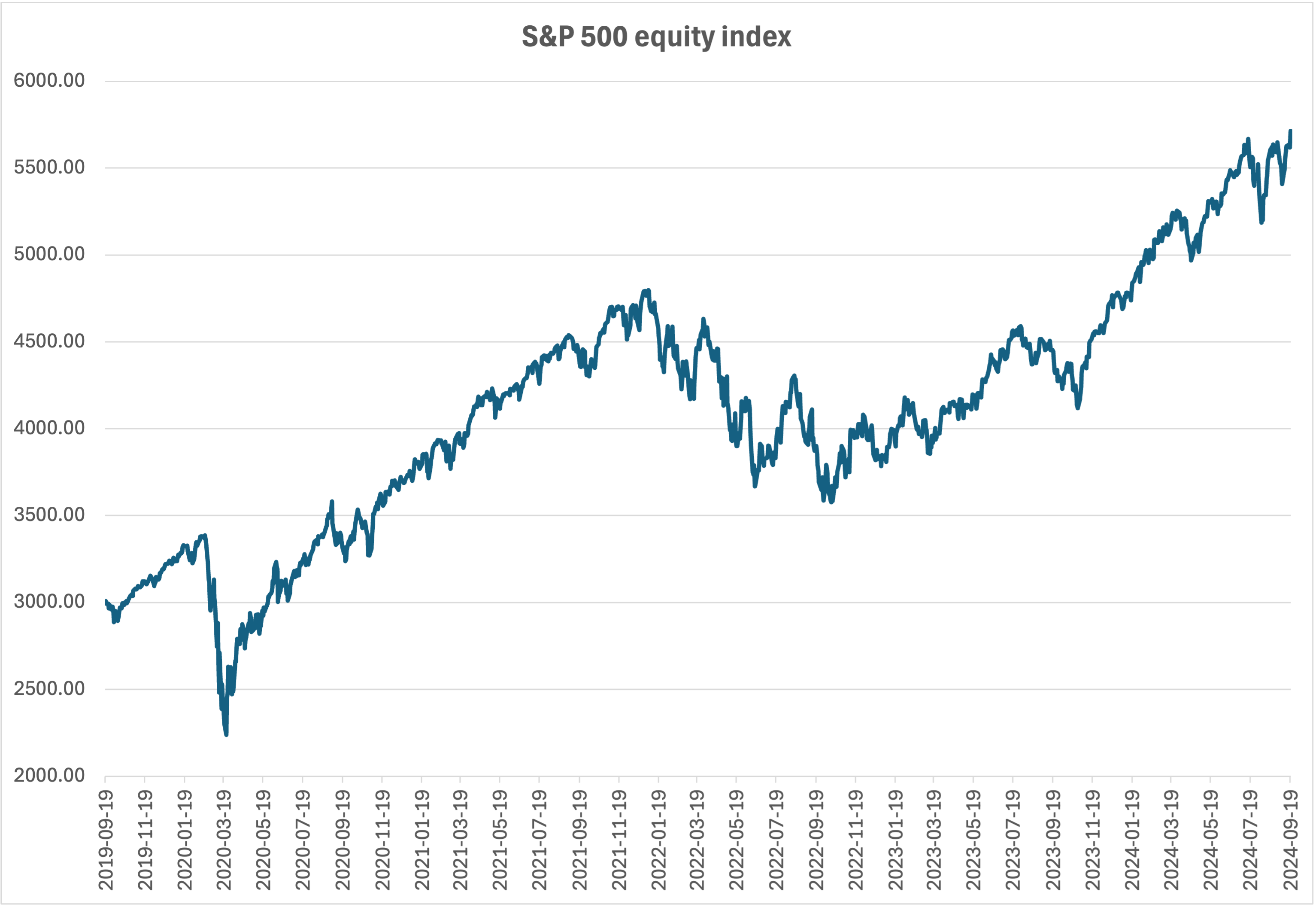

So does the stock market. In fact, judging by a simpler “follow the money” rule of thumb, financial markets do not seem all that worried that a recession might be on the horizon: equities trade at record highs, and spreads on risky assets are tight.

Source: S&P Dow Jones Indices via St Louis Fed FRED database

You think that’s normal?

A rate cut was still justified: inflation has come down significantly, and we can afford a looser monetary policy. But how much looser? It depends on what you think a “normal” economy looks like. Imagine a situation where the economy hums along at its potential growth rate, with full employment and inflation stable at its 2% target — what should the policy interest rate be?

Members of the Federal Open Market Committee (FOMC) — the Fed’s decision-makers — strongly disagree on this one. Their individual forecasts for such “neutral” policy rate range between 2.4% and 3.8% — almost 1.5 percentage points apart. (“Neutral” being the level of the policy rate that neither stimulates nor slows the economy.)

The dovish end (2.4%) would imply a real policy rate (nominal rate minus inflation) close to zero. It reflects a view of the world where inflation has already been defeated, the price spike was entirely due to supply shocks, and “normal” is a world where inflation lies forever dormant and central banks can set rates at extremely low levels. Like the period following the global financial crisis and through the pandemic, in other words. You think that’s normal? But markets share this view and think we’ll get there fast: they expect a policy rate well below 3% by the end of next year.

The hawkish end (policy rate ending close to 4%) would imply a neutral real policy rate close to 2%, in line with the long-term average prior to the global financial crisis.

If the dovish view is right, we have a lot of monetary easing to look forward to, and that’s clearly what financial markets anticipate. If the hawkish view is correct and the neutral rate is close to 4%, I hate to tell you but we’re almost there already (current policy rate is at 4.75%-5.0%).

Lest you think this is all irrelevant because we’re talking of a hypothetical future, Fed officials are equally divided on what do next year: all of them project for end-2025 an economy growing around potential, a labor market close to full employment and inflation close to target. Yet some FOMC members see this consistent with a policy rate below 3%, others with a rate above 4%.

Voodoo economics part II

Is there a way of telling which view is more likely correct? Powell is fond of saying that the neutral rate cannot be observed and “we only know it by its works.” I think if we were three percentage points about the neutral policy rate, the policy stance would be very restrictive and we’d see much slower growth and higher unemployment. The fact that we have full employment, above-potential growth and ebullient financial markets suggests policy is not that restrictive.

This also implies we should not stop worrying about inflation (and love the deficit). A new IMF paper shows that the high inflation of 2021-2023 was mostly due to excessively strong demand for goods and services boosted by loose monetary and fiscal policies — not by supply shocks. This should have been obvious: flush with savings and government subsidies and emerging from a long suspended animation, consumers started spending with a vengeance; governments fanned the flames with additional fiscal stimulus (especially in the US) while central banks financed it with an extremely loose monetary stance. Energy price shocks and supply chain disruptions provided the spark that ignited inflation, but not the fuel that kept it going at such high rates for so long.

In the US, fiscal policy is still very loose and will remain so for the foreseeable future, as I argued last week, because politicians still believe we live in a world without budget constraints, where you can print money and create prosperity from thin air — voodoo economics. With the economy already strong, this poses an obvious risk to inflation — and limits the scope for further monetary easing.

Sanity, please

The Fed September rate cut has opened a new phase in the painful journey back to normalcy after a decade and a half of madness encompassing a global financial crisis, a pandemic and the worst inflation in forty years. The optimistic view is that inflation risks have vanished and we have plenty of monetary easing to look forward to. The more sober view is that the scope for monetary easing is limited — especially given recklessly loose fiscal policy. I’m in the latter camp. Politicians and financial markets gravitate towards the wishful thinking camp. Fed officials are pragmatically trying to figure out what “normal” looks like. Wish them luck, and pray that markets and politicians will eventually take heed — there is a lot at stake.

Hi Marco: thanks for sharing your thoughts. It is indeed a very good overview of the key issues from a monetary policy perspective. I do see the debate centered around the destination of the policy rate in a scenario in which the economy is in some sort of ideal equilibrium (the most recent label is "equipoise"). You pointed out at the importance of fiscal policy and it is a bit surprising how that is out from the main monetary policy debate in terms of assessing for example its effectiveness. My view is that we are in a different regime, a regime of fiscal primacy. Finally I am a bit skeptical about the IMF paper's analysis. There is a good thread by V. Constancio on X (https://x.com/VMRConstancio/status/1808436550834798746) that provides some concerns on the analysis. Here is also one of the author's reply as well (https://x.com/gprimice/status/1811461250141827173).

Marco, this is an awesome read, thank you. I should have paid more attention in Econ class clearly! A couple of very basic questions:

1. Why do we celebrate 2 - 2.5% inflation so much? Isn't price the area under the inflation curve? So if something cost $1 3 years ago and we had 5 - 8% inflation for 3 years, it now costs $1.20 ish. Why would we not want "negative inflation" for a couple of years?

2. Cold hearted question about immigration: Let's say we deport x million undocumented immigrants. I would imagine there would be a hit on consumption (deflationary?) and a corresponding lowering of competition in the labor market (inflationary?) Do these balance out? Is one force stronger than the other?

Pardon the naivete in advance!

Sanjeev